Futures Rise After Trump Extends Ceasefire Even As Brent Tops $100

Futures are higher with earnings in full swing and AI winners soaring. Trump indefinitely extended the ceasefire with Iran just before its Taco Tuesday expiration, while maintaining a blockade of the Strait of Hormuz, after plans for peace talks fell apart. Still, the market doesn’t seem too concerned about the lack of a resolution, and is instead focused on a Tasnim report that Iran had received “some signs” the US was ready to break the blockade. As of 8:00am, S&P futures were up 0.6%, rebounding from two days of declines; Nasdaq futures gained 0.7% with all Mag 7 names trading higher in the premarket. The VIX traded around 19. Overnight, Brent briefly climbed above $100 a barrel as talks earmarked for Islamabad failed to take place, leaving the Strait of Hormuz mostly shut. Tensions escalated as Iranian tankers tested a US blockade and the UK Maritime Trade Operations said two ships came under fire. Treasuries rose across the curve, with the 10-year yield dropping two basis points to 4.27%. The dollar eased 0.1%, while Bitcoin headed for the highest level since February and gold/silver rebounding from yesterday’s weakness. There is nothing on the macro calendar but we will have another busy day with earnings: TSLA is expected to report after market-close today.

In premarket trading, Mag 7 stocks are again all higher (AMZN +1%, META +0.7%, MSFT +0.7%, GOOGL +0.7%, TSLA +0.6%, AAPL +0.4%, NVDA +0.6%)

- Cryptocurrency-linked stocks rally alongside Bitcoin and risk assets more broadly.

- Adobe Inc. (ADBE) rises 2% after saying it will buy back as much as $25 billion of its stock.

- Amneal Pharmaceuticals (AMRX) gains 2% after boosting its adjusted earnings per share forecast for the full year.

- ASM International (ASM) NV hit a high in Amsterdam on strong orders for the chip-equipment maker’s gear.

- Boeing (BA) climbs 4% after reporting lower-than-expected cash outflow as it delivered the most aircraft in the first quarter since 2019.

- Capital One (COF) slips 1% after the credit-card reported earnings for the first quarter that missed the average analyst estimate and set aside more cash to cover soured loans.

- GE Vernova (GEV) gains 7% after the power equipment company reported revenue for the first quarter that beat the average analyst estimate.

- Intuitive Surgical (ISRG) rises 2% after the medical equipment firm boosted its full-year forecast, with analysts citing strong worldwide procedure growth using its da Vinci system.

- Sonoco Products (SON) falls 6% after the containers and packaging company forecast adjusted earnings per share for the full year to be at the low end of its previously stated guidance.

- Twilio Inc. (TWLO) rises 6% after BofA upgraded the software company by two notches, to buy from underperform. The company “will not be disrupted by AI,” writes analyst Koji Ikeda.

- United Airlines (UAL) gains 2%, with travel stocks broadly higher, after President Donald Trump said he’s extending the ceasefire deal with Iran until talks conclude. Analysts largely dismissed the carrier’s reduced adjusted earnings-per-share forecast for the full year, noting that the updated guidance is not too far off from the consensus estimate.

- Vertiv Holdings (VRT) falls 4% after the power equipment company’s report was marred by “areas of disappointment,” which investors in the momentum name tend to fixate on. Organic growth fell short of expectations, as did a second-quarter profit view.

In corporate news, United Airlines slashed its forecast due to higher fuel prices caused by war in the Middle East, while Lufthansa will scrub 20,000 uneconomic short-haul flights from its European summer schedule. SpaceX said it has an agreement giving it the right to acquire AI startup Cursor, part of the Elon Musk-run firm’s efforts to catch up with rivals in AI coding tools. A small group of unauthorized users have accessed Anthropic’s new Mythos model, which the company says can enable dangerous cyberattacks.

Brent briefly climbed above $100 a barrel as talks earmarked for Islamabad failed to take place, leaving the Strait of Hormuz mostly shut. While a return to fighting the war is not on the cards, there is still little sign the critical Strait of Hormuz will be reopened to oil and gas shipments soon. Iranian gunboats fired on two ships in the waterway on Wednesday. Yet despite gains in oil, futures rose after the first back-to-back drop this month.

“Investors are either standing on the sidelines or have accepted the emotional influence on the market, knowing that negotiations to end the conflict are ongoing,” said Guillermo Hernandez Sampere, head of trading at MPPM.

“Markets are still navigating a fragile balance between improving sentiment and lingering geopolitical risk,” said Daniela Hathorn, senior market analyst at Capital.com. “While ceasefire headlines and periodic reopenings of the Strait of Hormuz have helped ease immediate supply fears, disruptions to flows continue to linger, keeping a residual risk premium embedded in energy markets.”

While stocks are again trading near record highs and earnings remain strong, some market participants warn that oil price volatility is likely to persist, with no deal in sight to reopen the Strait of Hormuz.

“Mixed messages from Donald Trump, and an insistence that a US blockade of Iran will continue, mean investors are still playing a guessing game,” said Russ Mould at AJ Bell. “Having tipped into alarm bell territory above $100 per barrel, oil prices have now dipped below this level – but they still tell a story of distress in global energy markets.”

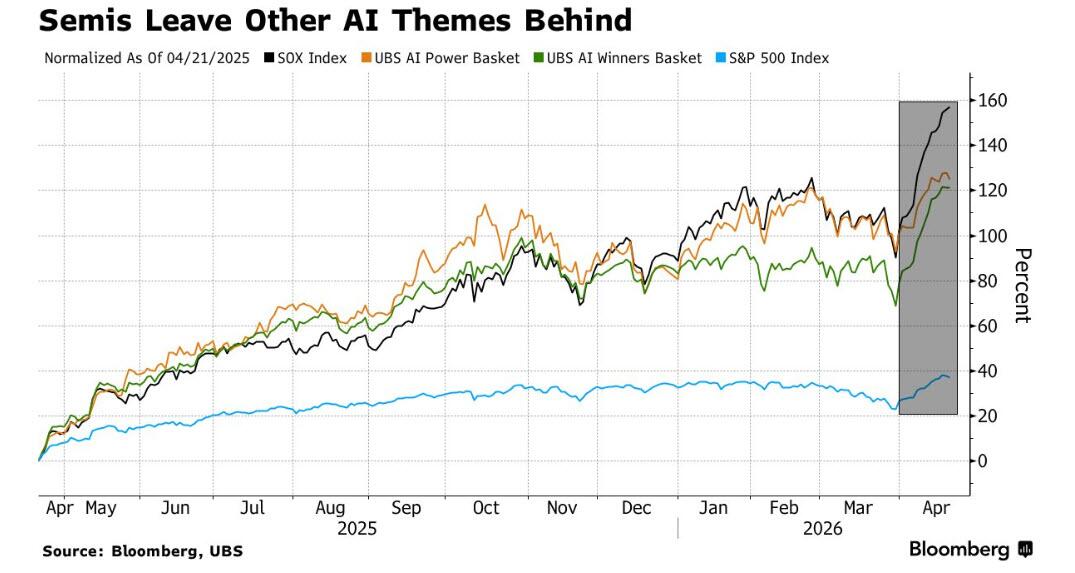

In tech, the Philadelphia Semiconductor Index eyeing its longest winning streak ever after 15 days of gains. Memory chip makers are riding surging demand to record profits, yet their stocks are still trading at a fraction of the valuation multiples of other top AI chip names. The shift of trader attention away from war-related risk to earnings is not just playing out on the single-stock level but also showing up in S&P 500 options. Tech earnings through the lens of options reflect a bigger event catalyst than weekend surprises around the conflict.

First quarter earnings season has been off to a strong start, with 82% of the 71 companies in the S&P 500 that have reported so far outpacing estimates. Investors have rewarded names linked to the AI in particular, as strong demand drives fresh optimism around the adoption of the capital-intensive technology.

Tesla will be the main focus of corporate results on a busy day for US earnings. A slate of chip names including Texas Instruments and Lam Research is also due to report.

In politics, Virginia voters backed a Democratic plan to redraw the state’s congressional districts in a way that could net them as many as four more US House seats in November’s midterms. Kevin Warsh’s future remains opaque as Trump has doubled down on a criminal probe that is effectively blocking his own nominee from taking over at the Fed.

European shares advanced, but erased much of an earlier gain with the Stoxx 600 rising 0.1% to 616.7 led by energy, after Trump indefinitely extended a ceasefire with Iran just before its expiration. Energy is the best-performing subsector, while travel and leisure shares are the biggest laggards. Technology stocks outperform after ASM International projected revenue for the second quarter that exceeded analysts’ estimates. Here are some of the biggest movers on Wednesday:

- ASM International shares rally as much as 9.5% and hit a record high after the chip-equipment maker gave an estimate-beating sales forecast for 2Q, while predicting 2H performance will be even stronger.

- ABB shares gain as much as 6.2% to a record after the Swiss power technology company raised its revenue expectations for the year on strong orders, in a move analysts called surprising and likely to drive consensus upgrades.

- Randstad shares rise as much as 7% after the recruitment company surprised the market by posting its first quarterly positive organic revenue growth in three years.

- Danone gains as much as 3.8% after the French foodmaker delivered in-line like-for-like sales growth in the first quarter, despite impact from an infant formula recall.

- Deutsche Telekom shares slip as much as 4% after Bloomberg News reported that the German firm is considering a full combination with its American arm T-Mobile US.

- Aberdeen shares rise as much as 1.7% to their highest in more than a month as the investment management company confirmed its full-year guidance despite market headwinds in the first quarter.

- Bureau Veritas shares fall as much as 13% after a cut to full-year organic growth guidance to the mid-single digits from mid-to-high single digits, following a weaker-than-expected 1Q performance.

- Akzo Nobel shares rise as much as 5.6% after results that analysts described as strong, especially within the context of the conflict in the Middle East and its impact on raw material prices.

- Moncler shares fall as much as 3% as the Italian luxury fashion brand’s first-quarter sales were overshadowed by high buy-side expectations and questions whether the company will be able to keep momentum up in the next quarters, according to RBC.

- Evolution falls as much as 5.4% after the Swedish online gambling firm reported earnings. Analysts say persistent weakness in Europe is the key disappointment in the report, balanced out by stronger performance in the Americas.

- Reckitt shares drop as much as 7% after like-for-like growth fell short of expectations, primarily due to a weaker-than-expected cold and flu season.

- Montana Aerospace shares fall as much as 10%, the most since April 7, after CEO Kai Arndt informed the Board of Directors of his intention to step down.

- European hearing-technology companies’ shares are under pressure after Cochlear, the Australian maker of implantable hearing devices, cut profit guidance, sending its stock plummeting the most in over 30 years.

Asian stocks declined, snapping a two-day win streak, as US President Donald Trump’s extension of a ceasefire with Iran failed to ease investor concerns after plans for talks between the two countries fell apart. The MSCI Asia Pacific Index dropped as much as 0.8%, with most industry groups in the red. Alibaba and Tencent were among the biggest drags as Chinese tech shares slumped. Equity gauges in Hong Kong led losses around the region, while Taiwanese stocks climbed. The MSCI Asia benchmark is still down about 2% since US and Israel launched the first attacks on Iran, while measures of US equities have erased their war-related losses to touch new records. Tech-heavy markets Taiwan and South Korea have rebounded to fresh highs recently on a resurgence of the AI trade.

In FX, The Bloomberg Dollar Spot Index falls 0.2%. The Norwegian krone is leading gains against the greenback, rising 0.7%. The yen and franc are little changed.

In rates, treasuries inched higher too, underpinned by oil prices only moderately higher on the day and wider rally seen across long-end gilts as markets continue to react to President Donald Trump indefinitely extending his ceasefire with Iran. Treasuries richer by broadly 1bp to 2bp across the curve with belly leading gains on the day, steepening 5s30s spread by almost 1bp and unwinding a small portion of Tuesday’s aggressive flattening move. US 10-year yields trade around 4.28%, down roughly 1bp vs. Tuesday close. Treasury auctions scheduled for the session include $13 billion 20-year bond reopening at 1pm New York. The WI 20-year trading currently at around 4.875% is ~6bp cheaper than the March reopening, which traded 0.7bp through the WI in a solid result.

In commodities, Brent crude futures briefly topped $100 barrel earlier today and remain within touching distance of that level as attempts to resolve the seven-week conflict between the US and Iran struggled. Iran seized two ships that “intended to secretly exit the Strait of Hormuz,” state TV reported. Earlier, the UK Navy said two ships were fired at near the Strait of Hormuz. Precious metals climb, with spot silver up 1.5%. Bitcoin rises 3%.

US economic data calendar slate empty for the session

Market Snapshot

- S&P 500 mini +0.6%

- Nasdaq 100 mini +0.8%

- Russell 2000 mini +0.9%

- Stoxx Europe 600 +0.1%

- DAX little changed, CAC 40 -0.2%

- 10-year Treasury yield little changed at 4.29%

- VIX -0.5 points at 19.01

- Bloomberg Dollar Index -0.2% at 1194.24

- euro little changed at $1.1752

- WTI crude +0.7% at $90.31/barrel

Top overnight News

- US President Trump is reportedly willing to Iran give another three to five days of ceasefire: “It certainly looks like Trump doesn’t want to use military force anymore and has made a decision to end the war,”. US officials and Pakistani mediators are waiting for Khamenei to break his silence in the next day or two and give his negotiators a clear directive to return to the table. Ceasefire is not going to be open-ended, the source added: Axios

- Two Ships Attacked in Hormuz After Trump Extends Cease-Fire, Blockade: WSJ

- Iran received ‘some sign’ the US is ready to break the blockade, Tasnim reported.

- Virginia Voters Narrowly Approve Measure to Boost Democrats in Midterms: WSJ

- Pakistani Journalist Mallick posted “To my understanding, while there might be some roadblocks for the second round of US – Iran in person talks to go ahead, but Diplomacy is not dead and its currently at play.”.

- Tables turn as Republicans face gas-price attacks they once used on Democrats: RTRS

- US President Trump posted “Iran is collapsing financially! They want the Strait of Hormuz opened immediately- Starving for cash! Losing 500 Million Dollars a day. Military and Police complaining that they are not getting paid. SOS!!!”.

- Fox News cited sources that stated US President Trump’s decision not to resume strikes on Iran for now is a last chance for peace that Trump is giving to the Iranian people, but added the ceasefire will be short-term unless an agreement is reached shortly.

Iran news

- UKMTO said it has received a report of an incident 8 nautical miles west of Iran; A master of an outbound cargo ship reported having been fired upon and is now stopped in the water, no reported damage.

- UKMTO said received information about an incident 15 nautical miles to the northeast of Oman in which a container vessel was approached by a single IRGC gunboat, while gunfire struck the vessel and severely damaged the bridge. said: There are no fires or environmental damage reported and the crew is safe.

- Pakistani Journalist Mallick posted “To my understanding, while there might be some roadblocks for the second round of US – Iran in person talks to go ahead, but Diplomacy is not dead and its currently at play.”.

- US President Trump is reportedly willing to Iran give another three to five days of ceasefire, Axios reported citing sources; “It certainly looks like Trump doesn’t want to use military force anymore and has made a decision to end the war,”. US officials and Pakistani mediators are waiting for Khamenei to break his silence in the next day or two and give his negotiators a clear directive to return to the table. Ceasefire is not going to be open-ended, the source added.

- Iran received ‘some sign’ the US is ready to break the blockade, Tasnim reported.

- US President Trump posted “Iran is collapsing financially! They want the Strait of Hormuz opened immediately- Starving for cash! Losing 500 Million Dollars a day. Military and Police complaining that they are not getting paid. SOS!!!”.

- Fox News cited sources that stated US President Trump’s decision not to resume strikes on Iran for now is a last chance for peace that Trump is giving to the Iranian people, but added the ceasefire will be short-term unless an agreement is reached shortly.

- US President Trump posted “Iran doesn’t want the Strait of Hormuz closed, they want it open so they can make $500 Million Dollars a day (which is, therefore, what they are losing if it is closed!)”. Full post “Iran doesn’t want the Strait of Hormuz closed, they want it open so they can make $500 Million Dollars a day (which is, therefore, what they are losing if it is closed!). They only say they want it closed because I have it totally BLOCKADED (CLOSED!), so they merely want to “save face.” People approached me four days ago, saying, “Sir, Iran wants to open up the Strait, immediately.” But if we do that, there can never be a Deal with Iran, unless we blow up the rest of their Country, their leaders included! President DONALD J. TRUMP”.

- Iranian Parliament’s National Security and Foreign Policy Commission member Khazarian said while Trump is announcing the end of the ceasefire unilaterally, at the same time he raised the maritime blockade, which is a ridiculous contradiction. said:. It means that both this is a military action and there is a silent war against Iran and expects that Iran will not respond and adhere to the ceasefire. This issue is not accepted by Iran.

- Iran top joint military command spokesperson said they are warning against repeated threats of the US President and army commanders, that their capable and the powerful forces have been 100% ready and on the trigger for a long time. said: In case of aggression and any action against Iran, they will immediately attack the predetermined targets and teach the aggressor, America and Israeli regime another lesson.

- Tasnim noted that continuation of naval blockade means continuation of hostilities, adds Iran will not reopen Strait of Hormuz until the maritime blockade continues and will break the blockade by force if necessary.

- Iranian TV states Iran will not recognize ceasefire announced by Trump and may not abide by it and will act in accordance with its national interests, according to Al Mayadeen.

- US blocks Iraq’s dollar shipments to squeeze its Iran-backed militias and suspends security cooperation with Baghdad in an escalating pressure campaign, according to WSJ.

- Iran’s Parliament Speaker Ghalibaf’s Advisor said Trump’s decision to extend the ceasefire makes no sense. The ceasefire extension is an attempt to buy time for a surprise attack. Iran currently holds the initiative.

- Pakistani PM is discussing with his ministers ways to persuade the Iranian side to return to the talks, Al Jazeera reported, citing sources.

- UK will host military planners from over 30 countries on Wednesday to develop a mission to reopen the Strait of Hormuz, according to The Times.

- US Secretary of State Rubio will join talks between Israel and Lebanon on Thursday.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed as participants reflected on the latest geopolitical developments, including the collapse of peace talks in Islamabad, while US President Trump announced an extension of the ceasefire until discussions conclude, but will maintain the naval blockade in Hormuz. ASX 200 declined with the index dragged lower by underperformance in health care and the top-weighted financial industry, while the mining sector was rangebound despite gains in BHP following its quarterly production update. Nikkei 225 initially clawed back losses and printed a fresh record high with some encouragement from stronger-than-expected Exports and Imports data from Japan, while recent source reports continued to point to the central bank refraining from hiking rates next week. Hang Seng and Shanghai Comp were mixed with the Hong Kong benchmark the underperformer, as tech weakness clouded over the strength seen in the Chinese oil majors, while the mainland was kept afloat in rangebound trade with very few fresh China-specific catalysts.

Top Asian News

- Australian Westpac Leading Index MM (Mar) -0.1% (Prev. -0.1%).

- Japanese Imports YoY (Mar) Y/Y 10.9% vs. Exp. 7.1% (Prev. 10.2%, Low. 3.8%, High. 10.1%).

- Japanese Exports YoY (Mar) Y/Y 11.7% vs. Exp. 11% (Prev. 4.2%, Low. 6.4%, High. 14.2%).

- Japanese Balance of Trade (Mar) 667.0B vs. Exp. 1106B (Prev. 57.3B, Low. 700B, High. 5306B).

- Korea (Republic of) PPI MoM (Mar) M/M 1.6% (Prev. 0.6%).

European bourses opened with very mild gains, but have slowly trundled lower as the morning progressed, alongside a slight pick-up in the energy complex. From an index stand-point, the IBEX 35 (-0.4%) lags vs peers, whilst the AEX (+0.6%) outperforms, lifted by post-earnings strength in ASM International (+8.5%). In brief, the Co. reported strong Q1 results, driven by AI demand and resilient Chinese sales; the Co. also provided upbeat guidance. European sectors now display a mixed picture, after initially showing a positive bias. Unsurprisingly, Energy tops the pile given recent advances in the complex, followed closely by Basic Resources and Chemicals. Gains across underlying metals prices, alongside an upbeat update from Australia’s BHP has lifted sentiment across mining names – Fresnillo (+2%) also extends higher after a mixed production update. As for the Chemicals sector, Akzo Nobel (+5%) jumps after topping earnings forecasts, and lifting prices to counteract supply-side issues.

Top European News

- POLITICO said no resignation watch rumors are yet circulating in Westminster DMs, referring to UK PM Starmer. Chancellor Reeves publicly backed the PM at last night’s Good Growth Foundation reception, POLITICO reported.

- UK pension funds were warned they face large costs if they attempt to offload private market assets, following a warning by the industry regulator about some schemes’ high exposure to hard-to-sell investments, according to FT.

Trade/Tariffs

- USTR Greer called for US allies to pay more for critical minerals and said a ‘security premium’ needed to counter reliance on Chinese supplies, according to FT.

Central Banks

- ECB’s Lane said countries could decide to finance investment in European-wide public goods through more common debt.

- ECB’s Kazaks said the central bank has the “luxury” of not needing to rush to raise interest rates and he sees no rush to respond to higher energy prices driven by Iran war, according to FT.

- BoE’s Breeden said private credit liquidity risk threatens stability.

FX

- FX trades mostly firmer vs the USD as oil prices chop either side of the unchanged mark following an extension of the US-Iran ceasefire.

- DXY trades lower by a tenth after being sold on a Bloomberg headline this morning, “Iran received ‘some sign’ the US is ready to break the blockade”, desk looked into the headline and found it was likely in relation to comments made by the UN Ambassador Amir Saeid Iravani on Tuesday. It seems other desks were notified of this, which saw a modest and gradual reversal of the downward move. DXY lost steam at its 100 and 200 DMA (98.50) on Wednesday, and currently trades at 98.32.

- Kiwi outperforms once again amid continued rate repricing for the RBNZ. Markets are now expecting the OCR to be raised by 85bps by year-end, with the first cut fully priced for July, and around 50/50 for the May 27th meeting. AUD/NZD trickled lower overnight and into the European morning, currently -0.2% despite Aussie holding up well amid firmer gold prices. NOK is the only currency outperforming the bird today, helped by continued elevated oil prices, the scandi cross is higher by 0.7% and looks to 7th April highs of 0.9883.

- GBP modestly weakened on March inflation data, which was as expected at a headline level, while the core figures were cooler, but the all-important services lifted from the prior by more than expected. Overall, the BoE will likely be willing to wait and see for more data at this stage, as the lack of overt second-round effects means they have time to assess and weigh the growth vs inflation situation. GBP/USD is higher by a tenth of a percent and remains on a 1.35 handle. Overnight, Cable attempted a move below the aforementioned level but faltered at the 1.3503 mark. EUR/GBP trades a touch lower. At the time of writing, the cross attempts new lows near 0.8684.

Fixed Income

- A marginally bullish morning, at first at least, for fixed after relatively contained overnight trade. Modest upward impetus came after the Tasnim piece regarding the Hormuz blockade; though, it does appear to be a re-run of remarks from Tuesday.

- The complex has come under pressure after a UKMTO report around a cargo ship incident 8nm from Iran; reacting to the upside in energy. However, this pressure has since mostly pared, with the complex edging off worst levels and back towards the unchanged mark.

- USTs got to a 111-13 peak after that report, then gradually faded to unchanged and to a 111-07+ low thereafter, with losses of two ticks at most vs earlier gains of 4+. For the US, the main scheduled event is the 20yr auction. However, focus will undoubtedly be on any update to the geopolitical situation; see the morning’s analysis piece for more.

- Gilts opened higher by 11 ticks, in line with the action in Bunds at the time. Thereafter, the benchmark climbed to a 88.08 peak with gains of 20 ticks at most. Upside also spurred in reaction to the morning’s CPI series, with the headline as forecast and the core figure cooler-than-expected. However, the all-important services lifted by more than expected vs the prior; albeit, that itself is somewhat caveated by the early Easter, and may be partially unwound in April. Overall, for the BoE, they will likely be willing to wait and see for more data at this stage, as the lack of overt second-round effects means they have time to assess and weigh the growth vs inflation situation.

- Bunds in-fitting with the general move. Hit a 125.81 peak with gains of c. 15 ticks before moderating and fading alongside the latest energy uptick.

Commodities

- In geopolitics, US President Trump said the US had been asked to hold its attack on Iran until Iranian leaders and representatives can come up with a unified proposal, and extended the ceasefire until such time as their proposal is submitted and discussions are concluded, one way or the other, while instructing the military to continue the blockade. Axios reported that Trump is willing to give Iran another three to five days of ceasefire, with one source saying it looks like Trump does not want to use military force anymore and has made a decision to end the war, while also stressing the ceasefire is not going to be open-ended. US-Iran talks remained in limbo, with VP Vance’s trip to Pakistan called off / postponed, Iran deciding not to attend Islamabad on Wednesday, and mediators still trying to get both sides back to the table. Iranian officials said the continuation of the naval blockade means continuation of hostilities, while warning that Tehran may not recognise or abide by the ceasefire under such conditions. In Hormuz, two separate reports were released by the UKMTO as Iran targets ships in the region.

- WTI and Brent futures are firmer as geopolitics remain the driving force, with uncertainty continuing to weigh on the supply side of the equation alongside reports of attacks on ships in the region. WTI resides towards the top end of a USD 87.64-91.41/bbl range, while its Brent counterpart trades in a USD 96.54-100.39/bbl parameter. Dutch TTF also trades modestly firmer north of EUR 42/MWh but well-off war-peaks.

- Precious metals are firmer as the DXY takes a breather from yesterday’s rise. Spot gold yesterday dipped under its 100 DMA (USD 4,730/oz) to a USD 4,668.62/oz low before trimming losses and rising back above the 100 DMA and to levels around USD 4,750/oz (USD 4,715-4,772/oz). Spot silver this morning found resistance at its 100 DMA (USD 78.68/oz), with the metal currently in a USD 76.70-78.68/oz band at the time of writing.

- Base metals are mostly firmer across the board to varying degrees, with a softer dollar underpinning price action for now, alongside some relief following Trump’s ceasefire extension, despite the breakdown of talks. 3M LME copper resides in a USD 13,213.33-13,335.00/t range at the time of writing.

- US Private Energy Inventories (bbls): Crude -4.5mln (exp -1.8mln), Distillate -4.6mln (exp. -2.5mln), Gasoline -5.2mln (exp. -1.3mln), Cushing +0.7mln.

- Japan has reportedly agreed to import 1mln bbls of crude oil from Mexico, due to arrive in July, Nikkei reported. Comes as Japan seeks to reduce reliance on the Middle East after supply concerns linked to the de facto closure of the Strait of Hormuz. Japan and Mexico leaders also discussed broader energy and economic security cooperation, including critical minerals and supply chains.

- Fire reported at an oil refinery in Erbil, Iraq, Al Hadath reported.

- Slovak Economy Minister said Druzhba flows via Ukraine to Slovakia expected to restart on Thursday morning.

- Fujairah, UAE crude inventory at 7.45mln barrels, a five-year low.

- Hungary’s MOL said it received notice from Ukrtransnafta of its readiness to resume oil deliveries via Druzhba, TASS reported.

- Hungarian officials have told Politico that a decision on the EU loan to Ukraine is dependent on actual flows through the Druzhba pipeline.

- Kazakhstan Energy Minister said that they do not intend to reduce oil output following the suspension of exports to Germany.

- European Commission will unveil a package of measures today aimed at offsetting surging energy prices, according to Reuters.

- US President Trump considers extending waivers to ease US oil shipments, according to Axios.

- Ukraine is to resume Druzhba oil supplies on Wednesday afternoon.

Geopolitics

- Slovak Economy Minister said Druzhba flows via Ukraine to Slovakia expected to restart on Thursday morning.

- Ukraine’s Foreign Minister said they want a meeting between President Zelensky and Russian President Putin, have made enquiries to see if Turkey could host this.

- Hungarian officials have told Politico that a decision on the EU loan to Ukraine is dependent on actual flows through the Druzhba pipeline.

- Ukraine is to resume Druzhba oil supplies on Wednesday afternoon.

US Event Calendar

- 7:00 am: United States Apr 17 MBA Mortgage Applications 7.9%, prior 1.8%

DB’s JIm Reid concludes the overnight wrap

In the latest series of decisions that can be associated with a prolonged mid-life crisis, yesterday my new Whoop and Aura ring arrived where I’m going to use them to track my sleep and fitness/recovery levels to supplement my trusted Apple Watch. I’m still trying to digest the first night data. It said I had a sleep efficiency of 86% whatever that means. I know I woke up two or three times so that seems reasonable. Happy to receive tips from any experienced sleep tracker. Maybe every morning I’ll disclose my sleep efficiency so you can adjust your algorithms for any tiredness/irritation bias to the text.

Nearly 20 years of early starts on the EMR haven’t been great for sleep but the main news overnight occurred just before UK bed time and just after the US close with Trump’s statement on social media that he would be extending the ceasefire with Iran until Iran submits a new proposal “and discussions are concluded, one way or the other.” The US President cited “the fact that the Government of Iran is seriously fractured” as the reason for the extension but added that the US would continue its blockade against Iran. So that removes what had been a “Wednesday evening” deadline set by Trump, even if we’re yet to formally hear if Iran will abide by the ceasefire extension. The impending deadline had weighed on markets yesterday with concern mounting amid news that Iran had refused to take part in a new round of negotiations, leading Vice President JD Vance to postpone his planned trip to Islamabad.

Trump’s ceasefire extension has led to some recovery in markets overnight after bonds and equities lost ground on both sides of the Atlantic yesterday. But the breadth of the reversal this morning is relatively narrow, with more energy exposed regions underperforming. S&P futures (+0.51%) are seeing a sizeable rebound, on course to reverse most of the -0.63% S&P 500 decline yesterday, which marked the first back-to-back decline for the index in three weeks. However, those on the STOXX 50 are down -0.24%, while Asian equities are mixed.

Brent crude (-0.31%) is slightly lower this morning at $98.17/bbl after a +3.14% rise yesterday amid continued push back against the more optimistic tone from last Friday as the Strait of Hormuz remains largely closed. That leaves oil prices around the levels early in Friday’s session, before US and Iranian officials’ comments on reopening Hormuz drove de-escalation hopes. Meanwhile, 10yr Treasuries (-0.2bps after +4.1bps on Tuesday) and the dollar (0.0% after +0.30%) are seeing small moves overnight.

Speaking of oil, our strategist Michael Hsueh has raised his Q2 oil forecast to $96/bbl, before falling back to $87/bbl in Q3 and $78/bbl in Q4, aligning with a May re-opening scenario for the Strait of Hormuz. You can see his full note here.

Whilst the Middle East was still dominating attention, the focus also turned back to the Fed yesterday, as it was Kevin Warsh’s nomination hearing to become Fed Chair. There weren’t any huge surprises from that, but Warsh sought to reiterate his independence, saying that he wouldn’t be the President’s “sock puppet” and that “Fed independence means everything to me”. On policy, Warsh acknowledged that the Fed faces some “tough decisions” ahead. He argued rates could be lower if the balance sheet were smaller, but with no clear timeline on this, while striking a critical note on forward guidance and calling for a “regime change” in Fed communications. He also said that the Fed needed a new framework for addressing inflation, but he didn’t get into the specifics of that.

While that was going on, it’s worth noting that Republican Senator Thom Tillis reiterated his position that he’d vote against any Fed nominees until the Department of Justice probe into Chair Powell is over. That’s crucial because the Republicans only have a 13-11 majority on the Committee, so Tillis’ opposition could hold up Warsh’s nomination. So there’s still an outstanding question as to when Warsh might actually be confirmed, and if that would be in time for the end of Powell’s current four-year term on May 15. It might actually suit both the Administration and Warsh for his term to start after the Iran war is over so he can begin with a fresh slate rather than make the difficult decisions while uncertainty prevails.

In the meantime, Treasury yields moved higher during Warsh’s hearing, although that seemed to coincide as much with the oil gains rather than anything Warsh had said. So with inflation fears rising again, investors grew more doubtful that the Fed would still be able to cut rates this year, with the probability of a cut by December down to 34% by the close from 54% the previous day. Moreover, the 2yr yield (+5.8bps) was up to 3.78%, and the 10yr yield (+4.1bps) rose to 4.29%.

That rise in yields had begun even before the move higher in oil, following a strong batch of US economic data. This included March retail sales, which grew by a monthly +1.7% (vs. +1.4% expected). While this headline nominal increase came in larger part due to the rise in gasoline prices, the measure that excludes autos and gas also rose by a solid +0.6% (vs. +0.3% expected), showing consumer resilience despite the energy shock. And we saw stronger labour market data as well, with the ADP’s weekly report of private payrolls rising to a new series high of 54.75k for the four weeks ending April 4, while pending home sales (+1.5% vs +0.5% expected) were also solid in March.

Despite the stronger data, US equities struggled yesterday, as Iran fears and the prospect of a more hawkish Fed served to dampen sentiment. So the S&P 500 gave up its initial gains at the open to close -0.63% lower. This marked the S&P 500’s worst day since March 27, with a broad-based fall that saw two-thirds of the index lower on the day. Energy (+1.31%) was the only major sector group to advance. The decline also came despite some positive earnings, including from UnitedHealth Group (+6.96%) as they raised their outlook.

Earlier in Europe, markets underperformed given the region’s greater exposure to energy, with the STOXX 600 (-0.87%) seeing a sizeable decline, alongside a rise in 10yr yields for bunds (+2.2bps), OATs (+4.5bps) and BTPs (+5.2bps).

Here in the UK, continued speculation over UK PM Starmer’s position saw 10yr gilts (+5.1bps) continue to underperform most of their

European counterparts. That followed a hearing appearance by Oliver Robbins, previously the most senior civil servant in the Foreign Office, who was fired by Starmer for not informing him that former US ambassador Peter Mandelson had failed security vetting. However, Robbins said that the PM’s office had a “dismissive approach” and there was an “atmosphere of pressure” created. So that led to mounting speculation about a leadership challenge against Starmer, which has been a concern for markets given expectations that a new PM might ease the fiscal rules and lead to higher gilt issuance.

That move for gilts got further momentum from an unexpected drop in UK unemployment, which fell to +4.9% in the three months to February (vs +5.2% expected). Otherwise, we also had Germany’s ZEW survey for April, where the expectations component fell to -17.2 (-5.8 expected).

Coming back to Asia, markets are quiet and not particularly benefitting from the ceasefire extension. The Nikkei 225 (+0.16%) is edging to a fresh record high while the KOSPI is flat around its all time highs. In other markets, the CSI (+0.30%) and the Shanghai Composite (+0.24%) are also witnessing small gains but the Hang Seng (-1.32%) is sharply lower with the S&P/ASX 200 (-0.98%) not far behind.

Early morning data showed that Japan’s exports have increased for the seventh consecutive month, driven by strong global demand and rising prices, and currently showing resilience against significant disruptions caused by the conflict in the Middle East. The total value of exports rose by 11.7% year-on-year in March, surpassing the market expectation of an 11% increase. Imports also saw a rise of 10.9% in March compared to the previous year, exceeding the anticipated growth of 7.0%. Consequently, Japan achieved a trade surplus of 667 billion yen in March, in contrast to the forecast surplus of 1.1 trillion yen.

To the day ahead now, we have a big batch of UK data including March CPI, RPI, PPI. We’ll also get the Eurozone April consumer confidence survey, as well as hear from the ECB’s Lagarde, Lane, Nagel, and Slejpen. Earnings include Tesla, Lam Research, IBM, Texas Instruments and Boeing.

Tyler Durden

Wed, 04/22/2026 – 08:36