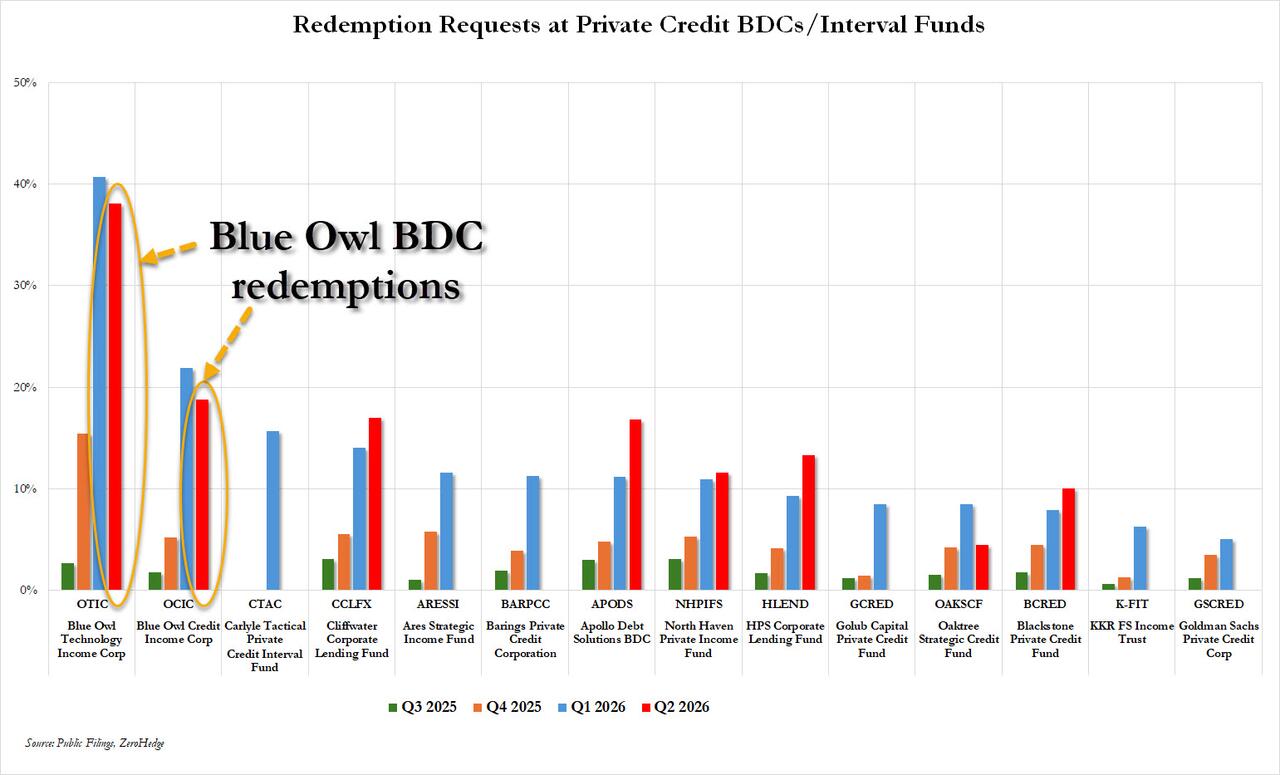

Blue Owl Gates Investors Again After Top BDCs Hit With Massive 38%, 19% Redemption Requests

After a catastrophic Q1 for private credit BDCs, Q2 is proceeding just as many had expected: just as bad.

After alternative asset manager titans such as Apollo, Blackrock, Blackstone and Cliffwater all gated their investors for a second straight quarter following a surge in redemption requests that easily surpassed what took place in Q1, earlier today we learned that the ground zero of the private credit implosion – Blue Owl Capital – was also slammed with redemption requests in the second quarter. Sure enough, it also gated its investors.

As Bloomberg reports, for the second straight quarter, two Blue Owl Capital private credit funds were hit with the industry’s largest redemption requests, forcing the manager to again cap withdrawals.

Investors in the roughly $34 billion Blue Owl Credit Income Corp., one of the largest in the industry, asked to pull 18.8% of shares, or $3.6 billion in the second quarter, according to an investor letter Thursday. That’s down fractionally less than the $4.2 billion requested in the prior period from the fund known as OCIC.

The smaller Blue Owl Technology Income Corp. saw shareholders request 38.1%, or $1.1 billion, compared with $1.2 billion in the first quarter.

The good news: the total redemptions were modestly below last quarter’s record; the bad news: the redemptions persisted almost entirely despite the market staging a historic, remarkable rebound and as fears about software disruption supposedly eased. Turns out they did not.

Blue Owl, which as we have thoroughly documents, has been at the heart of the storm roiling the $1.8 trillion private credit market due to its massive exposure to software-linked loans, joins industry peers including Apollo, Ares, BlackRock and Blackstone in imposing a 5% redemption limit as investors accelerate out of the funds.

Blue Owl told investors it was “encouraged to see OCIC’s modestly lower quarter-over-quarter tender requests broadly across channels and geographies.” Let’s see what the company will tell investors next quarter if we see a powerful drawdown in stocks which sparks a new selling panic across the private credit space.

According to Bloomberg, the firm said it has satisfied more than 43% of the original demand from shareholders with repeat withdrawal requests. It said second quarter requests were largely from those investors, and included “limited new participation.”

Realizing the existential threat they were in, Blue Owl executives – who in a bizarre act of “diversification” decided to buy a stake in the Cleveland Cavaliers – stepped up efforts to engage with clients over the past three months, flying around the world on a roadshow trying to educate investors, according to a person with knowledge of the matter. They emphasized the message that private credit is a performing asset and that their funds had delivered positive returns, the person said, requesting anonymity to discuss private meetings.

In the shareholder letter Thursday, the firm highlighted that about 90% of investors remain in the larger fund, which has posted approximately $1.2 billion of inflows this year.

“OCIC does not need to sell a single private loan to satisfy the tender offer,” Craig Packer, Blue Owl’s co-president, and Logan Nicholson, OCIC president, said in the letter to shareholders.

And in case that investors decided they don’t want to be in the fund much longer, the firm said that both Blue Owl funds have “ample dry powder” to capitalize on better lending conditions in the market, with wider spreads and improved protections.

OCIC and OTIC had $11.6 billion and $1.3 billion in liquidity respectively, including cash and available borrowings assets as of May 31, according to the letters. OTIC oversees about $5 billion in assets.

Tyler Durden

Thu, 07/02/2026 – 14:20