“GPIF To The Rescue?” Yen Jumps After Japan Urges Pension Funds To Invest More At Home

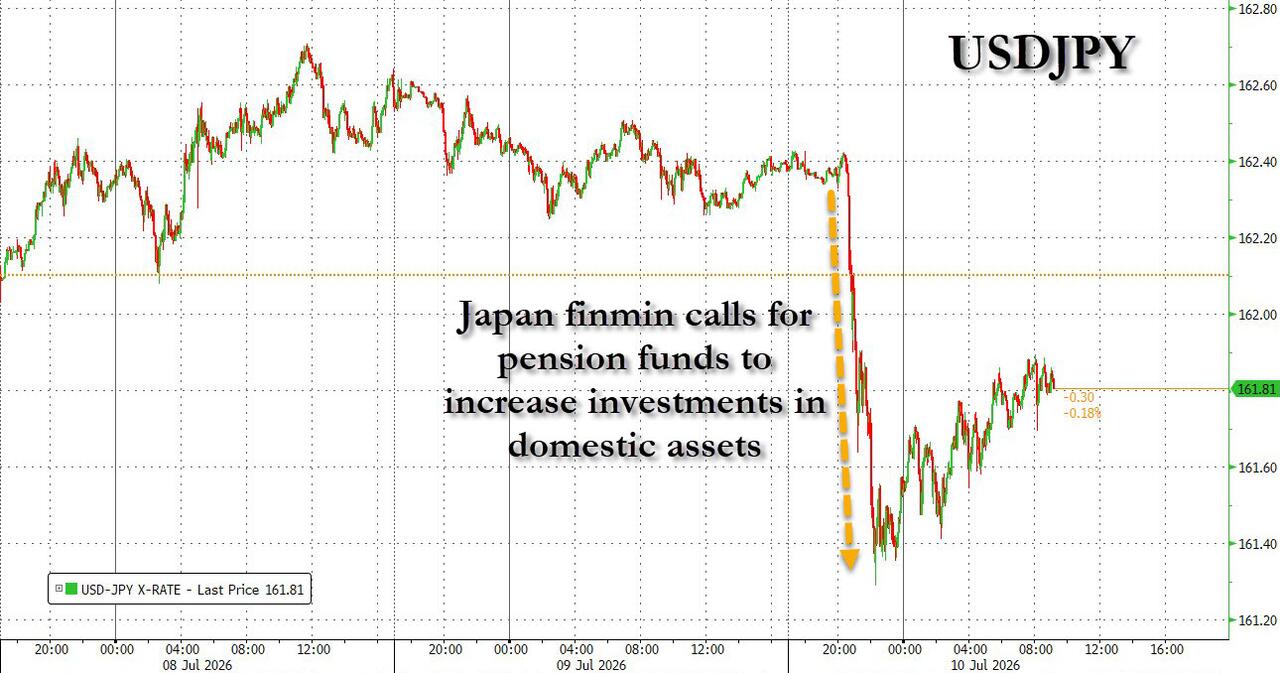

After a relentless collapse in the yen to a 40 year lows, the trajectory was finally dented overnight when Japan’s finance minister called for the nation’s massive pension funds to increase investments in domestic assets, boosting the yen from near four-decade lows and spurring a rally in bonds.

“One priority is to encourage households, as well as pension funds including the GPIF, to increase their investment in Japanese financial assets. We intend to pursue policies that support that objective,” Finance Minister Satsuki Katayama said Friday, referring to the Government Pension Investment Fund. It’s one of the world’s largest pensions with ¥293.6 trillion ($1.81 trillion) in assets.

The remarks in response to a question at a regular press briefing about government investment plans caught markets off guard, leading to a jump in the yen and a drop in bond yields. Both assets had been under considerable stress this week.

According to Bloomberg, Katayama’s comments on the GPIF were prepared in advance, citing a person familiar with the matter said. It’s unclear if they were intended to be form of verbal intervention, although they certainly impacted the yen more than the recent BoJ rate hike or ongoing currency jawboning.

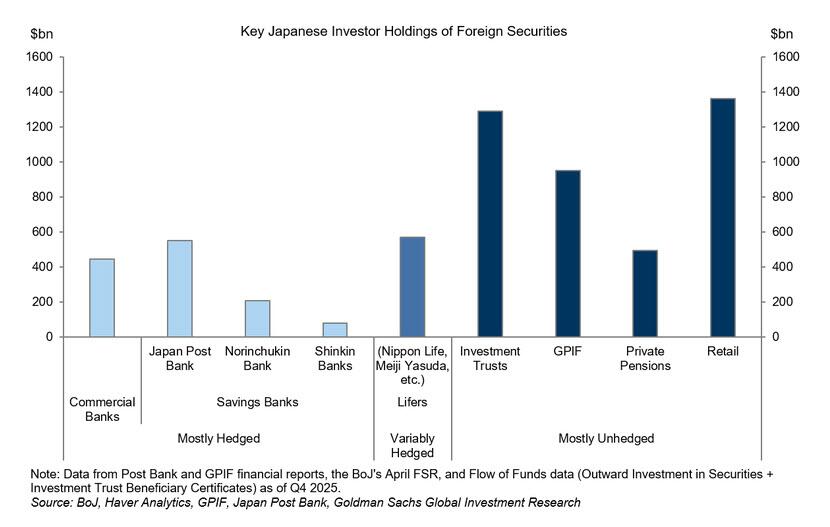

Japan’s giant GPIF pension fund is overseen by the labor ministry, not finance, and any changes to its investment strategy would have to go through an established process that would take time to implement. If any changes to allocations were to occur, the implications could spread beyond Japan. The nation is the largest foreign holder of US Treasuries with a $1.2 trillion stockpile, and almost $5 trillion of the country’s capital is deployed overseas.

Ironically, over the past decade, the big push domestically was for the GPIF to invest more abroad, especially in US equities, at a time when Japanese stocks languished for year after year. However, with the Nikkei now significantly outperforming the S&P, it is hardly a surprise that local authorities are pushing for another reallocation, this time from abroad back to home.

Katayama’s comments were in response to a question on how the government’s plan to increase investment in strategic areas, such as artificial intelligence, would benefit its people. Prime Minister Sanae Takaichi unveiled a plan last month for ¥370 trillion to be invested in the economy over the course of 14 years, with more than a quarter of it earmarked for AI and chips alone.

“We want to ensure that the public can directly benefit from Japan’s economic growth,” Katayama said.

The Takaichi administration is a well-known proponent of accommodative monetary policy. An early draft of its economic policy guidelines released last month fanned market worries that the government is trying to exert influence over the BOJ, prompting several revisions to tame concerns. Katayama also said on Friday that monetary policy should be handled by the BOJ.

The call to reallocate investments signals the government’s intention to channel more household and institutional savings into domestic assets as the nation enters a new phase of economic growth accompanied by positive interest rates. Japanese equities have performed strongly this year, with the Nikkei 225 recently climbing above the 70,000 mark for the first time.

While it’s not clear how seriously the government is considering the issue, a reallocation of funds toward domestic investment would be a boost for the yen near 40-year lows. Besides rate-differentials with the US that have weighed on the currency, the yen has also been under pressure from capital outflows and concerns about the Bank of Japan’s independence.

In immediate response to the comments, the yen strengthened to as firm as 161.29 per dollar before paring some gains. Bonds rallied, with yields across the curve declining about 10 basis points.

GPIF’s potential changes “cannot be ignored” given the size of its assets under management, said Yugo Tsuboi, chief strategist at Daiwa Securities. Katayama’s comments “could help sustain a ‘triple rally’ of bonds, the yen and stocks in the Japanese market.”

Some market participants doubted whether the comments will lead to any changes in asset allocation.

However, some traders doubt whether the comments will lead to any changes in asset allocation.

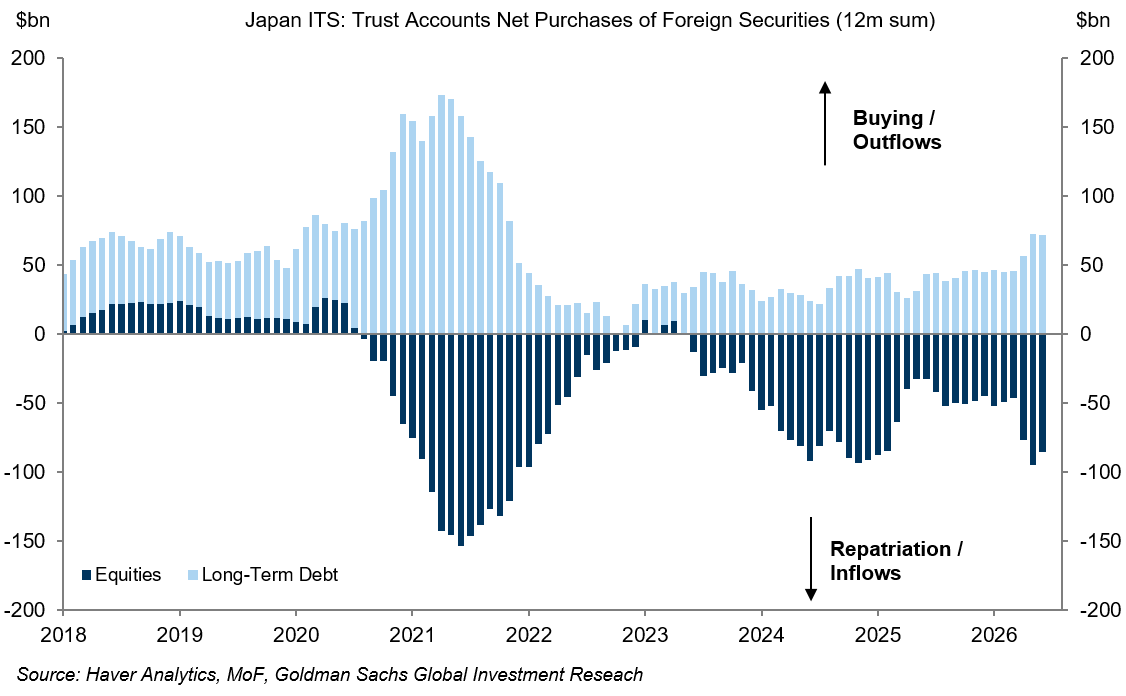

In a note from Goldman’s FX team titled “The Scope for Japanese Repatriation Flows” (available to pro subs), the bank cautions that the comments do not signal an actual shift in government policy. Their framing is that meaningful repatriation flows, if they occur, would be one of the more credible paths to the yen correcting its severe undervaluation – while noting investor anticipation of such flows has repeatedly picked up over the past year (e.g., after the snap election) without materializing.

“We have long been skeptical of the scope for significant JPY-positive repatriation flows without a more favorable rate differential, especially since GPIF also has a return target that it needs to achieve. But any meaningful reallocation back towards domestic assets should be a source of support for the Yen, in addition to any rise in recession risk or more aggressive BoJ hikes” wrote Goldman strategist Karen Reichgott Fishman

In a separate note titled “GPIF to the Rescue?”, Goldman said that Katayama’s remarks sparked a JGB reversal rally, with 5y+ JGBs richening 5–11.5bps, but here too the bank’s stance was skeptical, calling the rally “an overreaction,” and noting that the FinMin used the broad term “Japanese financial assets” and did not explicitly commit GPIF to buying JGBs in size. They maintain a structurally bearish bias on ultra-long JGBs ahead of 20y/40y supply, and don’t see this as a structural turnaround.

Others agreed: “The macroeconomic backdrop has not changed, so it is difficult to see the yen strengthening for long,” said Kazushige Kaida, head of FX sales at State Street Bank & Trust Co.’s Tokyo branch. “If the latest comments suggest that the government is simply looking for ways to ease the pain of its reflationary policy, rather than abandoning it, then the broader story of yen weakness remains intact.”

The GPIF sets asset allocation parameters every five years. In March 2025, the fund decided to keep splitting a quarter of its funds equally between domestic stocks and bonds, foreign equities and debt. The fund also cut the maximum deviation from the target to 5-6 percentage points depending on movements by the various asset classes, from 6-8 percentage points.

GPIF posted its third best annual return on record in the 12 months ended March 31, according to a statement earlier this month. About half of the fund’s assets are invested overseas. The combined assets under management of Japan’s four public pension funds, led by GPIF, total about ¥332 trillion.

A shift “toward Japanese financial assets would be positive for Japanese equities,” said Yukihiro Kawanishi, a senior strategist at Aizawa Securities. “It could also encourage overseas investors, who have already moved ahead of the trend, to increase their allocations.”

Tyler Durden

Fri, 07/10/2026 – 09:40