Micron Earnings Preview: “Sentiment Is 11/10”

Micron, which is report earnings after the bell, has become one of the most important stocks in the world. The price has risen explosively recently, adding more than 260% this year. Yet the frenzy that drove it higher is looking extremely fragile, meaning there’s a lot riding on today’s earnings report.

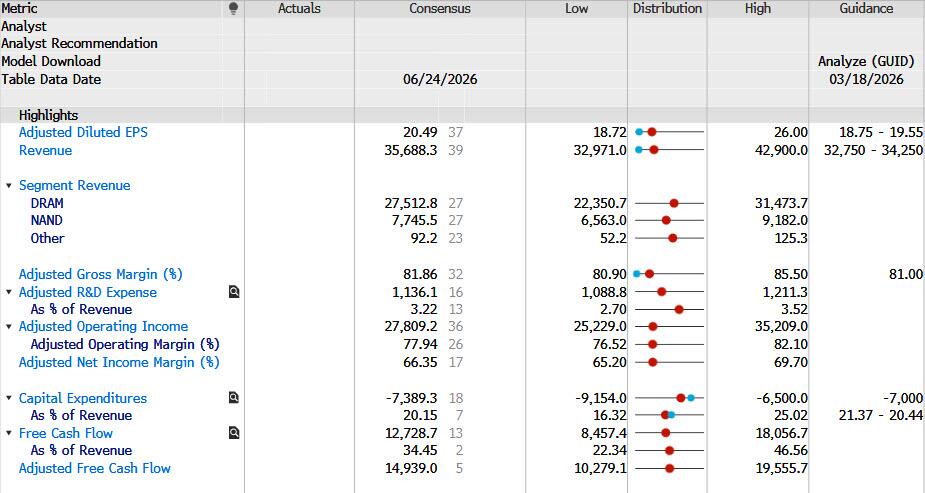

Before we drill down, here is a snapshot of what Wall Street sellside consensus expects for the current May, or fiscal Q3 quarter:

- Adj EPS: $20.492

- Revenue: $35.688BN

That said, buy-side expectations are well above, as high as $38 bn in revenue and $22.00 in EPS versus consensus at $35.68 bn and $20.49.

- Goldman expects revenue/GM/EPS of $37.6bn/83.4%/$22.07

Going down the line, here are some more consensus expectations:

- Adj Net Income: $23.563BN

- Operating Profit: $27.809BN

- EBITDA: $30.942BN

And visually:

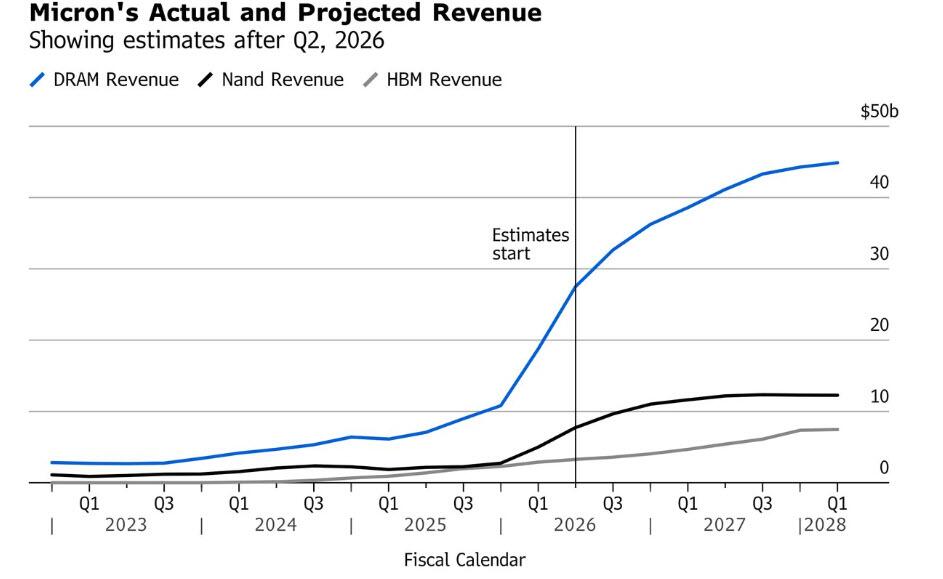

Micron makes memory, and its specialty is DRAM, fast, powerful, temporary memory that forgets things when the power is turned off, but it also makes NAND, slower memory that saves data. High-bandwidth memory (HBM) involves stacking DRAM in layers with a processor chip. It’s a subset of DRAM, so the numbers in the chart below add up to more than 100% of Micron’s total sales. The latest flavor of HBM is HBM4, which is a key ingredient of Nvidia’s newest generation of GPUs for AI. Only three companies make HBM4 for Nvidia and Micron is one of them.

As Bloomberg notes, if Micron’s guidance Wednesday shifts chip sales expectations higher, or pushes back the forecast slowdown in growth, that could give new life to the market’s enthusiasm for semiconductor stocks. The chart shows analyst projections for Micron’s sales of DRAM, NAND and HBM. Growth is seen slowing next year, after accelerating to more than 200% year-on-year this year.

Bank views:

UBS

Micron reports after the US close with sentiment stretched into the print, with MU carrying roughly 10% implied volatility and a 11/10 sentiment skew. Tim Arcuri reiterates Buy while lifting the price target sharply to $1,625 from $535, now the Street high, driven by a pathway to EPS above $100 and a more durable long-term earnings framework.

The core of the bull case is the structural shift created by long-term agreements across the memory industry. Supply chain work suggests up to 30% of DDR volumes could soon be locked in at pricing only slightly below current levels, allowing Micron to trade some near-term upside for materially improved demand visibility and a smoother earnings profile. This underpins a step-change in forward estimates, with C2027–2029 EPS raised to $155/$167/$117 from $133/$122/$77 previously, while EPS is expected to remain comfortably above $100 throughout the period. The framework implies more than $400 bn in free cash flow generation across the same timeframe.

With visibility improving, the multiple story becomes central. The desk notes increasing conviction that the market will begin to assign a more “normal” semiconductor multiple as earnings durability becomes clearer, supporting a continued re-rating as AI-driven structural changes across the memory complex are better understood. The new price target is based on roughly 15x NTM P/E applied to discounted C2029 EPS, marking a shift away from prior sum-of-the-parts methodology.

Into the print, the set-up is defined by a tension between very strong fundamentals and crowded positioning. While recent channel checks point to upside risk, with some buy-side expectations for fiscal Q3 as high as $38 bn in revenue and $22.00 in EPS versus consensus at $35.6 bn and $20.57, the key risk is messaging. Specifically, how management communicates the evolution of LTAs and balances near-term revenue trade-offs against longer-term stability will likely determine whether the stock can extend its re-rating from already elevated expectations.

Goldman

MU preview (Peter Callahan): Stock is lower 5 of 6 prints on t+1, supporting a view this is less of an “earning stock” relative to other AI names. Goldman’s James Schneider sits ~20%+ above the street for the August quarter, with Goldman ests Revs of ~$48.7bn (+30% q/q) and EPS of ~$29.95/shr vs cons $23.70 in F3Q).

From Goldman’s James Schneider; “We expect investors to continue to focus on the nature of Micron’s Strategic Customer Agreements (SCA), as well as supply plans and near-term pricing dynamics. We expect ongoing market tightness to drive significant upside to Street estimates and the company’s guidance, and we raise our estimates and price target. Given ongoing demand increases plus near-term supply constraints, we recently increased our overall industry outlook in our latest global report, and we expect tight conditions to persist throughout CY27 and to result in increased pricing and margins for the industry, including Micron. We believe investor positioning remains very bullish given the dramatic share price run-up and optimism around the potential impact of long-term customer agreements. We expect investors to focus on: (1) additional disclosure on SCAs, whether more agreements have been reached, and their specific features; (2) sustainability of pricing growth and industry undersupply in DRAM; and (3) target share level in HBM and ramp of HBM4 shipments..“

View on key metrics and our estimates: Goldman expects Micron to deliver ~9% upside to Street revenue in the quarter and guide to meaningful QoQ revenue growth in the August quarter, driven by pricing upside; expect revenue/GM/EPS of $37.6bn/83.4%/$22.07 for the quarter vs. Street at $34.4bn/81.9%/$19.74. For August quarter guidance, GS expect revenue/GM/EPS of $48.8bn/86.1%/$29.95 compared with Street at $40.4 bn/84.0%/$23.68. For CY26, Goldman’s revenue/EPS estimates are 30%/36% above the Street..

Estimate changes: Goldman raises its revenue/non-GAAP EPS estimates by 28%/36% on average for CY26/27 to reflect stronger industry pricing trends and demand upside.

Setup heading into the print: Investor expectations are very elevated heading into the print, with Micron benefiting from robust DRAM pricing trends; Investors expect Micron to maintain/expand its current ~20% share in HBM, with conventional DRAM pricing driving upside.

Items on the call that could move the stock: (1) Additional details on SCAs – We believe investors expect more color on Micron’s strategic customer agreements, what level of pricing guarantees they contain, and whether additional agreements have been reached; (2) Sustainability of pricing strength – We expect further color on whether the current DRAM pricing trend can sustain itself in the coming quarters; (3) HBM roadmap – We expect Micron to comment on its market share in HBM, and whether it can improve that position with HBM4.

Coming out of the print: Goldman expects the stock debate to continue to center primarily on long-term customer agreements and the sustainability of DRAM pricing strength; any future commentary regarding HBM progress and share targets will be in focus.

JPMorgan

MU Earnings Buyside Bars (from Josh Meyers):

The company reports Wed ~4pm, with the call to follow at 4:30pm ET and the open analyst call at 6pm (they are one of the few to open their sell-side analyst call for all to hear, and it’s often a revealing call). Memory has been one of the most consensus AI longs, and it remains not only one of our most crowded longs in tech, but indeed across our entire book (though it’s actually been higher in recent months). The demand picture continues to improve (most recently with the unexpected boom in agentic CPU demand), with the ASP trajectory seemingly rising with every new company meeting/check. Demand destruction is real, but for now the supply response is only modest.

Expect the key focus point of the call to be on how much higher the team sees AI applications driving ASPs (and what that means for GMs, which are already uncomfortably north of 80%). An important part of that will be the trends in Strategic Customer Agreements (SCAs, their new parlance for Long Term Agreements), of which they had negotiated only one last quarter; will there be more, and what terms will be revealed. Memory company SCAs (peers are also negotiating them) are meant to be 3~5 year DDR & NAND agreements – with up-front payments and financial commitments – that apparently comprise fixed volumes and negotiated price (fixed for the first part of the contract, variable for the rest); it remains unclear how much disclosure we’ll get on these instruments, and how much comfort we’ll get that buyers won’t still walk away in a downturn.

Judging from consensus EPS expectations through F28 (and into F29, based on a lot of my conversations) folks are optimistic about demand and SCAs, pointing to an unprecedented, elongated cycle and incredible FCF generation (there’s a world where they generate 30% of current market cap in free cash by end-28). The key concern I hear is how to value the stock in this new world. We’ve long argued for an EPS-based upcycle valuation, and that’s now clearly consensus, but some do express concern about not wanting to pay much more than 7~8x earnings.

In terms of my Buyside Earnings Survey, there was a strong consensus (~75%) that the MU team will announce additional SCAs; only a small minority (~10%) believe the company will hold off, citing a near-term focus on pricing leverage or ongoing negotiations. Expectations were split on % of forward bit shipments covered, with ~50% expecting that confirmation of SCAs but with no specific % disclosure (other than some saying possibly qualitative color on customer type, e.g., hyperscalers) and ~40% offering a specific % estimate, with a wide range but clustering around 30–50% of forward bit shipments.ASP expectations were pretty much in-line with consensus: 44.6% for DRAM and 45.9% for NAND.

More available to pro subs.

Tyler Durden

Wed, 06/24/2026 – 15:03