Micron Soars After Reporting Blowout Earnings, Boosts Guidance

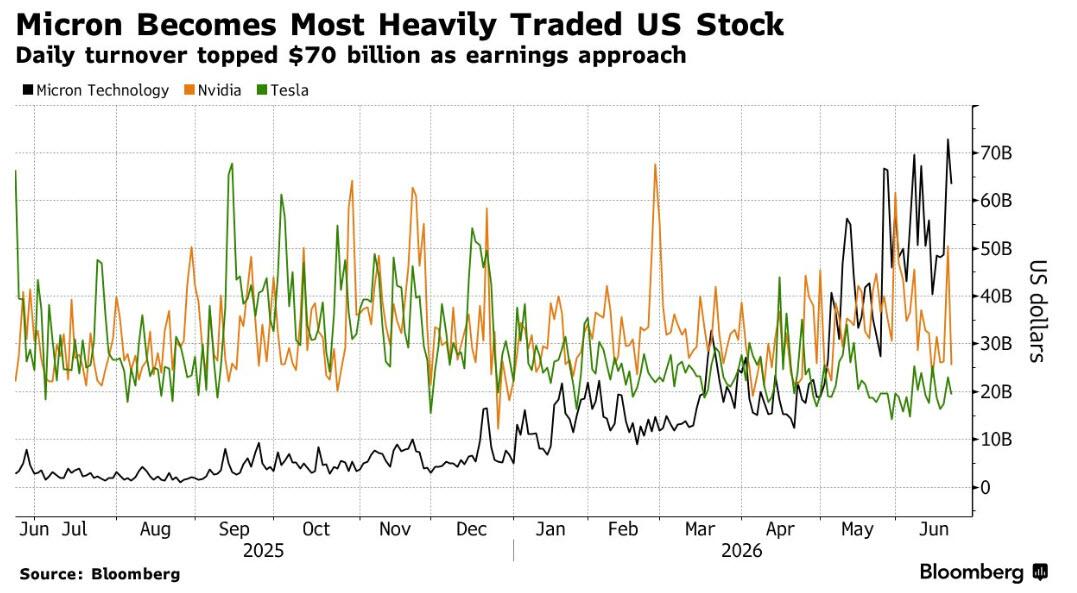

Step aside Nvidia: as we noted in our preview, with the world’s most valuable company going nowhere in recent months, all attention has shifted to Micron, which has rapidly become one of the most important stocks in the world and certainly the most actively traded, surpassing both Nvidia and Tesla in recent days.

As such all eyes were on Micron’s earnings today, and even with sentiment at 11/10, according to UBS, the company still managed to blow away expectations. Here is what it just reported for the just concluded May/Q3 fiscal quarter:

Starting with the bottom line…

- Adjusted EPS $25.11, beating consensus of $20.49.

We then go to the top of the income statement:

- Adjusted Revenue $$41.46BN, smashing all sellside estimates of $$35.69BN, and even well above the most optimistic buyside bogeys.

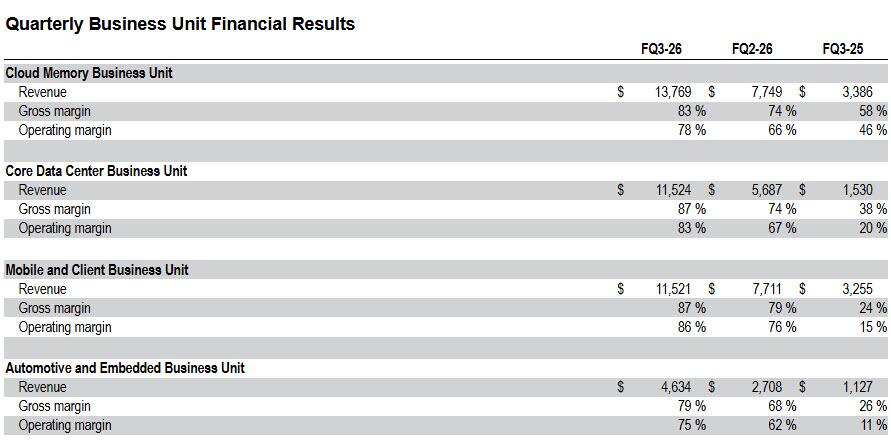

- Cloud Memory revenue $13.77 billion, beating estimate $10.69 billion

- Core Data Center revenue $11.52 billion, beating estimate $6.8 billion

- Mobile and Client Revenue $11.52 billion vs. $3.26 billion y/y, beating estimate $9.73 billion

- Automotive and Embedded rev. $4.63 billion, beating estimate $3.51 billion

- Adjusted gross margin 84.9% vs. 39% y/y, beating estimate 81.9%

- Adjusted operating income margin 81.2% vs. 26.8% y/y, beating estimate 77.9%

- R&D expenses $1.32 billion, +36% y/y, higher than estimate $1.29 billion

- Adjusted operating expenses $1.52 billion, +34% y/y, beating estimate $1.43 billion

Looking ahead, the company’s forecast is just as impressive:

- Micron sees Q4 adjusted Revenue of $49-$51BN, beating estimates of $43.24BN

- Sees adjusted EPS $30 to $32, beating estimate $25.31

- Sees adjusted gross margin about 86%, beating estimate 83.6%

- Sees adjusted operating expenses about $1.65 billion, below estimate $1.66 billion

Commenting on the quarter, the company said that “Micron is investing at record levels in technology, products and supply to address our customers’ rapidly growing demand. We believe our multi-year Strategic Customer Agreements will significantly enhance the durability and predictability of Micron’s strong financial performance.”

More important was the company’s discussion of its long-term agreements, i.e. “Strategic Customer Agreement”. This is what it said in the accompanying presentation:

- We are pleased to announce that we have completed 16 SCAs with customers across the data center, consumer and auto market segments. These SCAs accelerate the transformation of our business model, enhance partnership in technology and innovation, and provide customers with contracted supply assurance.

- Typically, these agreements have a five-year term, from calendar 2026 through the end of calendar 2030. Automotive agreements generally have a three-year term.

- The 16 signed agreements represent roughly 20% of our DRAM volume and a third of our NAND volume over this period.

- These SCAs include four very large customers and three medium-sized customers.

- The remaining agreements relate to smaller customers from the automotive industry and represent our commitment to this important sector.

- When completed, we expect approximately half or more of our company revenue to be under these SCAs with customers across end markets. Our customers value our U.S. supply plans, and this is reflected in our SCAs.

- These SCAs are structured as take-or-pay agreements, with binding commitments to purchase specific volumes over this multi-year term.

- The largest agreements generally have a ceiling price for existing products at the current CQ2 (calendar Q2) market price, and a floor price through the term of the agreement.

- Several SCAs, which account for a modest portion of the SCA-related revenue, include either fixed prices or have no price bands associated with them where pricing will be subject to market conditions. When all planned SCAs are executed, agreements with either fixed prices or price ceilings at or close to current CQ2 market prices are expected to be approximately 40% of our revenue.

- For SCAs which do contain such price bands, pricing is designed to stay within this floor to ceiling level through the course of the term. This pricing visibility will help our SCA customers across market segments to better manage their business and grow their demand.

- For our SCAs with price bands, the floor price enables a very robust gross margin for Micron, well above our peak quarterly margins in any past cycle.

- 14 of the 16 SCAs that we have signed have a cumulative revenue at minimum price per our contracts of approximately $100 billion over the remaining agreement term.

- They also strengthen our long-term financial performance, margins and free cash flow expectations, with higher visibility and improved stability in our business performance.

- Under the SCAs we have signed so far, we project to receive cash deposits and related financial commitments of $22 billion. This further demonstrates customer commitment to this new business model. Mark will provide additional details.

- Our SCAs with customers across data center to consumer devices to auto and industrial applications create a new paradigm for us to strengthen our customer relationships. They provide committed DRAM, including HBM as appropriate, and NAND supply to our customers over a multi-year time horizon.

- In a period of significant shortage, this supply visibility is extremely beneficial to our customers. This visibility enables our customers to leverage SCA supply to make progress on their strategic plans, drive growth and enable their end consumers to benefit from their products and services. We are very appreciative of our customers, who have worked with us through this period of tight supply with a strong collaborative spirit to create win-win outcomes for the long term for the entire ecosystem and end consumers.

In kneejerk response, the stock which slid in the past 2 days, has recovered most of the losses and has surged more than 10% rising to $1136 after briefly dipping below $1000 just before the market closed.

The company’s investor presentation is below (pdf link)

Tyler Durden

Wed, 06/24/2026 – 16:19