Stocks Drift As Chips Extend Gains, Oil Slides On Positive US-Iran Talks

Futures are modestly lower coming off the US holiday weekend, after equities finished higher last week with both Dow and Russell clocking new ATHs and SPX finishing in the green for the 11th time in the last 12 weeks. As of 8:00am ET, S&P 500 futures edged down 0.1% while Nasdaq 100 contracts are higher by 0.1% with chips outperforming as usual while hyperscalers, aka “check payers” down as all Mag 7 are lower with TSLA (-1.4%) and GOOGL (-1.6%; Google’s DeepMind VP John Jumper is leaving the company to join Anthropic) being the biggest laggards. Overseas, Asian markets mostly higher overnight with China and Japan the big gainers, up over 1.5%. European markets higher, up ~0.3%. Big development over the weekend revolved around US-Iran talks in Switzerland, where both sides ultimately highlighted progress following some earlier headline noise. Donald Trump again threatened strikes on Iran if Hezbollah keeps attacking Israel, & US and Iran set up a communication line to avoid incidents and ensure safe passage of shipping through the Strait of Hormuz. In the UK, PM Keir Starmer announced his resignation outside 10 Downing Street. The pound erased losses after briefly touching a 2026 low, while gilts rallied as an orderly leadership transition took shape. Bond yields are 2-4bp higher, while the USD is largely unchanged. WTI crude fell $-0.58 to $75.27 reversing all earlier gains while Brent traded around $79. Gold and silver are higher as is bitcoin. There is little on the corporate calendar and scant macro data, leaving traders with little direction until Micron’s earnings due Wednesday and the Fed’s preferred inflation gauge on Thursday take center stage. Fed speaker slate includes Waller at 9am; Williams, Goolsbee, Kashkari and Barkin speak later this week

In premarket trading, SpaceX shares slid more than 5% in premarket trading, putting the stock on pace for a third straight loss. Meanwhile, the semi meltup continues: chipmakers including Intel rallied. Getty Images soared more than 300% after inking a display partnership with ChatGPT owner OpenAI. Here are the notable premarket movers:

- Alphabet (GOOGL) -1.7%, Tesla (TSLA) -1.3%, Amazon (AMZN) -0.8%, Nvidia (NVDA) -0.2%, Meta Platforms (META) -0.9%, Apple (AAPL) -0.8%, Microsoft (MSFT) -0.4%

- Apogee Therapeutics (APGE) climbs 48% after AbbVie agreed to buy the company for $10.9 billion to bolster its anti-inflammatory portfolio amid growing competition for its best-selling drug.

- Arcosa (ACA) gains 7% after CRH said it has signed an agreement to acquire 100% of the provider of building materials in an all-cash transaction for $150 per share.

- Definium Therapeutics (DFTX) gains 32% after announcing positive topline results from a Phase 3 study evaluating a single dose of an orally disintegrating tablet in adults with major depressive disorder.

- Fervo Energy (FRVO) gains 8% after the geothermal-energy company agreed with Pacific Northwest National Laboratory and Nvidia to develop a digital twin platform for Enhanced Geothermal Systems technology.

- Getty Images (GETY) soars 156% after the company announced a display partnership With OpenAI.

- Regenxbio (RGNX) climbs 8% after the Wall Street Journal reported that the FDA has agreed to reverse the rejection of the firm’s rare-disease drug.

- SpaceX (SPCX) is down 5%, putting the stock on pace for a third straight loss.

A peppering of M&A and ECM news is spicing up an otherwise quiet Monday morning. Budget airline EasyJet has rejected three offers by US private credit giant Castlelake. AbbVie is closing in on a nearly $11 billion deal to buy inflammatory disease drug developer Apogee Therapeutics, according to the FT, which also reports that building materials group Arcosa could be close to a takeout by larger rival CRH. SpaceX kicked off its debut US dollar high-grade bond offering expected to be at least $25 billion.

The big geopolitical development over the weekend revolved around US-Iran talks in Switzerland, where both sides ultimately highlighted progress following some earlier headline noise. Oil traders took comfort from evidence of progress in Middle East talks even as President Donald Trump threatened to strike Iran if Hezbollah militants continue to attack Israel. Vance said the warring sides set up a mechanism to keep the Strait of Hormuz open, while Iran agreed to invite nuclear inspectors.

“Even during the midst of the conflict in the Middle East, equities still priced a positive outcome,” said Stephan Kemper, chief investment strategist at BNP Paribas Wealth Management. “It seems logical that markets don’t rally too hard on something which they had already priced to a fair degree.”

Traders also followed the latest developments in UK politics as Prime Minister Keir Starmer announced his resignation outside 10 Downing Street. The pound erased losses after briefly touching a 2026 low, while gilts rallied as an orderly leadership transition took shape. The departure of Starmer is putting Britain on course for its seventh premier in a decade and paving the way for Andy Burnham to replace him. The former mayor of Manchester announced his candidacy hours after Starmer’s resignation and received the backing of Wes Streeting, a potential rival. Starmer said nominations for a new Labour leader will open July 9 and that a contest will be finalized by Sept. 1. The question for investors is about the impact on the UK’s finances if Burnham were to become prime minister. A slew of all-but-forgotten niche option positions betting on an oil glut are coming back into play as crude cools.

“Markets would be watching for Burnham’s pick of Chancellor,” wrote Mohit Kumar at Jefferies. “The fear is that Burnham’s policies are left-leaning and if the new chancellor is not credible, it would raise concerns over deficits and borrowing.”

The AI trade still works and investors should keep it, say Goldman Sachs traders in charge of thematic investing, baskets and equity structuring.

In geopolitics, China has imposed export controls against US rare earth firms, in response to the Pentagon’s accusations against some of China’s biggest companies supporting the Chinese military.

Meanwhile, Trump’s administration is rolling out new tools with the same protectionist goals after the Supreme Court ruled his sweeping global tariffs to be illegal. The rising cost of living, and corruption, are shaping up to be major campaign battlefronts in races that will determine control of the US Congress.

Bond traders, recently forced to reposition for the possibility of higher interest rates ahead, are looking to Thursday’s US personal consumption expenditures price index for a read on whether the market’s hawkish stance is warranted. Forecasters expect the index, the Federal Reserve’s favorite inflation gauge, to show acceleration on both a monthly and year-over-year basis in May. Fed Governor Christopher Waller is due to speak later on Monday. Bloomberg Economics’ head Anna Wong expects a hot PCE reading will likely reinforce the hawkish tilt by the Fed at its June meeting.

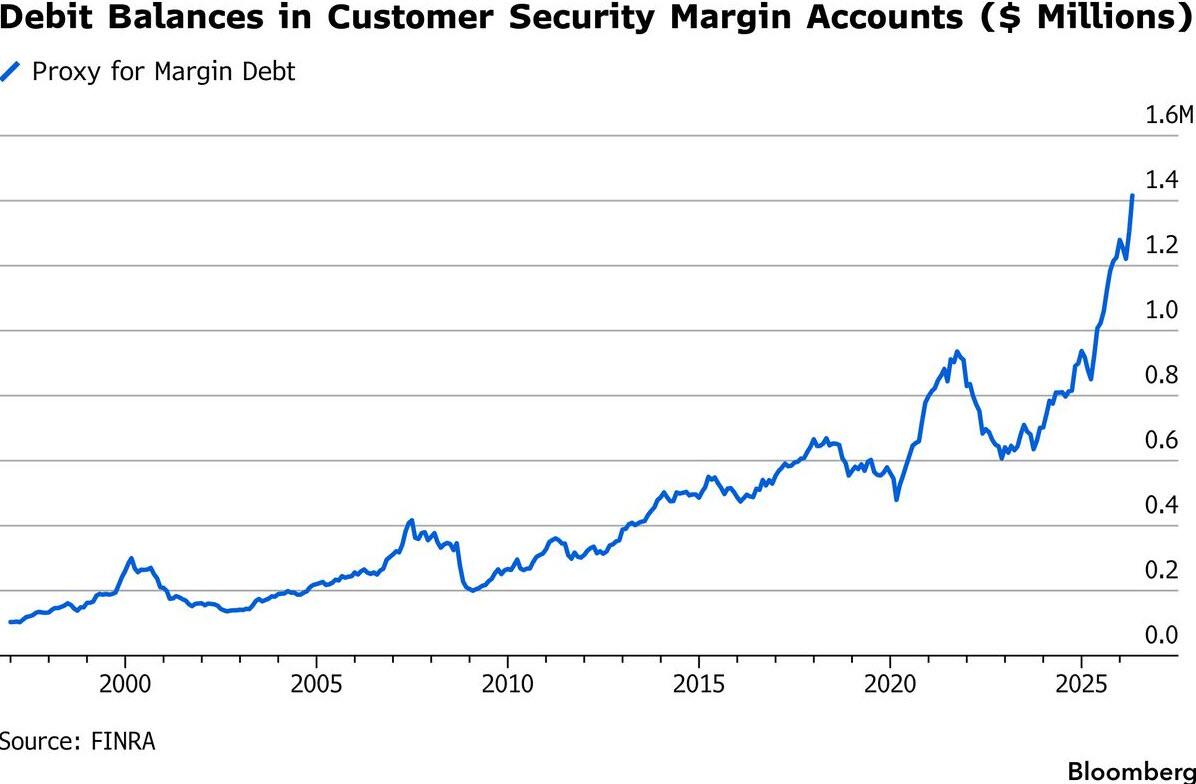

Ahead of Micron’s earnings, a leveraged ETF linked to rival SK Hynix is lifting an option cap. Rising leverage is also showing up in FINRA’s margin debt statistics, and the Roundhill DRAM ETF has recorded 19 straight days of inflows and AUM surpassed $20 billion. Micron’s fiscal 3Q revenue may exceed consensus by about 13% and guidance by 18%, notes BI.

European stocks struggled to derive much benefit with the Stoxx 600 down 0.1%, with construction and media stocks leading declines, while technology and energy shares are the biggest outperformers. Here are the biggest movers Monday:

- Infineon shares rise as much as 5.3%, after CFO Sven Schneider maintained his bullish stance on the chipmaker’s growth over the next few years, while Bernstein increased its price target for the stock

- EasyJet shares rise as much as 5.4% to the highest level in almost a year after the British budget carrier rejected a third takeover proposal from US investment firm Castlelake

- BioArctic jumps as much as 10%, the most in more than four months, after the Swedish biopharma company signed a research and collaboration agreement with Eli Lilly for its BrainTransporter technology

- LISI gains as much as 7.6%, reaching a record high, as Berenberg initiates on the component maker with a buy rating, citing entrenched positions in automotive and aerospace fasteners

- Sanofi shares slip as much as 2.1%, making them the biggest laggard by index points in the Stoxx 600’s healthcare subgroup on Monday morning

- Babcock shares fall as much as 5.7%, the most since February, as the defense contractor posts full-year results

- UBS shares are slide as much as 0.6%, falling for a second straight session after being downgraded at Zuercher Kantonalbank on valuation grounds, with the Swiss bank having hit a fresh 2008-high last Thursday

Asian stocks surged to a record as chipmakers and other artificial intelligence-linked firms rallied amid optimism surrounding US-Iran peace talks. The MSCI Asia Pacific Index rose as much as 1.1%, with information technology the top performing sector. Markets in Taiwan, mainland China and Japan led regional gains. Continued interest in AI and semiconductor plays drove Taiwan’s benchmark to a record high. South Korea’s memory maker SK Hynix also rose to an all-time high on expectations over its planned ADR listing, helping to erase earlier losses in the Kospi gauge. Meanwhile, equities in Hong Kong underperformed, as weak consumption data weighed on sentiment and investors chased the AI rally elsewhere. A gauge of Chinese stocks listed in the city was headed for a bear market before trimming some losses.

“We continue seeing liquidities leaving ‘old Techs’ in Hong Kong including Tencent, Alibaba and Baidu to chase AI-related stocks in Japan, Korea and Taiwan,” said Steven Leung, executive director at UOB Kay Hian.

In FX, the pound is down a handful of pips near its year-to-date low. The yen is the weakest of the G-10’s, falling 0.3% against the greenback.

In rates, treasuries decline, pushing US 10-year yields up 3 bps to 4.48% as trading resumes after Friday’s US cash-market holiday. US yields are 2bp-4bp higher on the day with losses led by front-end tenors, flattening 2s10s and 5s30s by 0.5bp and 1.5bp respectively. 10-year around 4.48% is cheaper by 3bp with bunds and gilts in the sector outperforming by 5bp and 6.5bp. European bonds outperform led by gilts after Wes Streeting backed Andy Burnham to be new UK Prime Minister, removing a key uncertainty after Keir Starmer’s resignation. Oil trades lower on signs of diplomatic headway between the US and Iran. IG dollar issuance slate includes a few items so far. Dealers forecast about $50 billion of US investment-grade bond sales this week, likely to include a jumbo bond offering from SpaceX. Treasury auctions resume Tuesday with $69 billion 2-year notes, followed by 5- and 7-year note sales Wednesday and Thursday

In commodities, Brent crude futures fall 1.6% after Iran said there had been “major progress” in all-night discussions with the US. WTI crude oil futures are down 0.8% near session lows after US Vice President Vance says Hormuz is open and talks with Iran have made progress. Precious metals advance, with spot silver rising 2%.

US event calendar: US economic data calendar empty for the session. Fed speaker slate includes Waller at 9am; Williams, Goolsbee, Kashkari and Barkin speak later this week

Market Snapshot

Top Overnight News

- The U.S. and Iran made progress during talks in Switzerland on Monday toward reaching a final deal within 60 days, including the agreement to establish a committee and a mechanism to end hostilities in Lebanon. CNBC

- The US and Iran set up a communication line to avoid incidents and ensure safe passage of shipping through the Strait of Hormuz. BBG

- UK PM Keir Starmer announced his resignation and outlined plans for a successor to take office by September. The move clears the way for Andy Burnham to become Britain’s seventh PM in a decade. Former Health Secretary Wes Streeting said he backed Burnham to become PM. The pound hovered near its weakest level of the year while gilts were little changed. BBG

- China announced on Monday that it will add 10 American firms to its export control list, including two rare earth firms, while also restricting 46 US firms from government procurement, signalling it would respond to Washington’s recent expansion of a military blacklist, even amid a broader stabilization of bilateral ties. SCMP

- South Korea’s exports jumped again in early June, thanks to AI fueling a sustained boom in the semiconductor sector. BBG

- Chevron signed a 20-year deal with Microsoft to supply natural-gas fired power to a planned West Texas data center that may become one of the largest in the US. BBG

- Semis are on pace to finish as the most net bought global subsector for a second straight year, with net allocations now at record highs. GS Prime Brokerage

- Major investors warned that Fed Chair Warsh’s push to axe the Fed’s guidance on the direction of monetary policy could increase volatility in the Treasury market and drive borrowing costs higher: FT.

- Hong Kong is in talks with Chinese authorities to expand cross-border investment channels and grant mainland buyers access to local IPOs. BBG

- Colombia elected Trump ally Abelardo de la Espriella president by a razor-thin margin. The preliminary result was immediately challenged by outgoing President Gustavo Petro, who backed rival candidate Senator Iván Cepeda. BBG

- US Secretary of State Rubio congratulates Colombia’s presidential candidate De la Espriella who leads against leftist rival Cepeda following the Colombian election.

- Democrats are set to make corruption a major campaign battlefront in the midterms as polling suggests voters are eager to see lawmakers take on conflicts of interest and self-enrichment by leaders. BBG

- US Southern Command announces that Task Force Southern Spear has conducted a strike on a vessel operated by designated terrorist organisations in the Caribbean.

- US Secretary of State Rubio plans trip to the Middle East next week: Kuwait, UAE and Bahrain at the moment: Axios

- US President Trump told Axios that he doesn’t see Anthropic PBC as a national security threat, despite his administration recently taking steps to cut off foreign access to the tech company’s most advanced AI models. Furthermore, Trump said that it was seen as a threat last week, but relations have improved since with the AI giant.

- US Department of Agriculture announced three new cases of screwworm to take the total number of domestic detections to 15 cases.

Iran Headlines: Latest News

- US and Iran talks opened in Switzerland on Sunday after US VP Vance arrived in Switzerland and the Iranian delegation led by chief negotiator Ghalibaf, which included Foreign Minister Araghchi, arrived on Saturday, while Pakistan’s Premier Sharif and military chief Munir travelled to Switzerland to join the US-Iran talks.

- Iran’s delegation reportedly left the negotiation site in protest against statements by US President Trump, while Fars also reported that Iran halted talks with the US after Trump threatened strikes over Hezbollah’s actions in Lebanon. Iran said Trump’s threat is a blatant violation of the MoU and halted talks in Switzerland, while it is reviewing a response to Trump’s threats. However, sources cited by Al Hadath later stated that the Iranian delegation had not left the negotiation headquarters at the Burgenstock resort and the Iranian delegation head discussed a joint statement draft with mediators.

- US President Trump threatened to resume bombing and take over the Strait of Hormuz if a deal is not reached, while Trump said the US may take tolls if it has to and that he has a 60-day option, in which he can do whatever after it. Trump stated he spoke with Iranian officials and used expletive language in the call with Iranian officials on Hormuz, as well as threatened that they won’t have a country if Hormuz is closed, according to Fox.

- US President Trump posted that Iran must immediately stop their proxies in Lebanon from causing trouble, or else the US would hit Iran very hard again, “just like we did last week, only harder!!!” Trump separately commented that there will be no tolls in the Strait of Hormuz, unless they are imposed by the US.

- UKMTO reported an incident in which a cargo vessel was approached by a craft with six armed persons onboard 92 nautical miles southwest of Yemen’s Mukalla in the Gulf of Aden.

- Israeli army chief said the Lebanon ceasefire is fragile and forces remain ready for combat.

- Israeli military convoy reportedly entered southern Syria’s Quneitra region, near the Israeli-controlled Golan Heights.

- Qatar and Pakistan issue joint statement on conclusion of US-Iran talks in Switzerland, while Qatar said first session of the US-Iran high level talks has concluded and that talks were conducted in a positive, constructive atmosphere. said:. Technical talks are to continue for remainder of the week. US and Iran agreed to de-confliction cell over Lebanon. Encouraging progress has been made, including creation of a mechanism for further technical talks. Parties agree to establish high-level committee to provide political oversight on mediation. High-level committee agrees on roadmap to reach final deal within 60 days.

- “The negotiations of the main Iranian delegation in Switzerland have ended, however, experts are still in Switzerland and are following up on the implementation of the memorandum of understanding”, Tasnim reported citing sources.

- Iranian negotiating team member said executive procedures about the release of Iranian frozen funds have taken place with the Qatari delegation and that a draft has been finalised regarding waivers of Iranian oil sanctions, which will be issued soon, although negotiations about other subjects will not take place if the war does not end in Lebanon.

- “No negotiations have taken place on the nuclear file so far”, Tasnim reported citing a source.

- US diplomat said talks included robust discussions on a nuclear deal and enforcing the ceasefire in southern Lebanon, while talks also involved clarifying the messaging on the Strait of Hormuz. Furthermore, a US official involved in the negotiations told Al Jazeera that they held in-depth discussions on all elements of the nuclear agreement, and that mechanisms have been worked on to prevent escalation and ensure the strait remains fully open.

- Pakistani Army Chief said negotiating parties reached success stage, according to Al Arabiya.

- US official involved in the negotiations told Al Jazeera that they held in-depth discussions on all elements of the nuclear agreement, adds mechanisms have been worked on to prevent escalation and ensure the strait remains fully open.

- Sources cited by Al Arabiya said an anticipated statement will be issued by the Iranian and American negotiators and the mediators.

- Sources cited by Al Hadath stated that the Iranian delegation has not left the negotiation headquarters at the Bürgenstock resort and Iranian delegation head discusses joint statement draft with mediators. Tasnim reported Iranian delegation refused to return to negotiations but message exchanges continue through intermediaries.

Iranian Commentary:

- Iran’s Foreign Minister Araghchi posted Pakistani and Qatari mediation delivered major progress to end Lebanon War, oil and petrochem exports are waived, blockade lifted, frozen assets released, and major reconstruction & development plan launched for Iran.

- Iran’s Foreign Ministry said the technical team is to continue work, but negotiation delegation work has concluded, adds significant progress achieved in quadrilateral talks in Switzerland. Spokesman said groundwork for starting negotiations for the final agreement was discussed.

- Iranian Foreign Ministry Spokesperson Baghaei said Iran is working on safe passage mechanism for Hormuz and that Iran reported progress on oil sales and asset unfreezing, adds the war in all fronts, including Lebanon, must end.

- Iranian Supreme Leader adviser Rezaei said the US is responsible for Israel’s actions in Lebanon and Iran will hold the US accountable in the event of a threat against Iran.

- Iranian Deputy Foreign Minister Gharibabadi to lead the technical team in Switzerland, Sky News Arabia reported.

- Iran resumed oil loading from Kharg Island after about a six-week halt, following the lifting of the US blockade of its ports.

Lebanon/Israel:

- Al Jadeed News cites Haaretz source stating the Israeli army will be forced to partially withdraw from the Blue Line in Lebanon.

- Israeli army will be forced to partially withdraw from the yellow line (buffer zone), Al Jazeera reported, citing Israel’s Haaretz sources.

- Israeli Foreign Minister Saar told his New Zealand counterpart, “Israel will respect the ceasefire in Lebanon as long as it won’t be breached by Hezbollah.”.

- Israeli political and security cabinet will convene on Thursday amid US-Iran talks, N12 reported.

- Israeli officials are dismissing reported of an agreement to withdraw from certain points in southern Lebanon, amid a lack of US pressure to do, Maariv’s Barsky reported. Officials add, “because in Washington they understand the Israeli position: no partial withdrawal, no point-specific withdrawal, and no diplomatic ‘gesture’.”. And, “as long as the Hezbollah threat persists, there is no change in the deployment of forces and no intention to relinquish the security positions in southern Lebanon.”.

- Lebanese presidency discussed the issue of consolidating the ceasefire in Lebanon, in a call with Qatari PM and US’s Vance.

Other:

- Two South Korean vessels were said to have passed through the Strait of Hormuz after US and Iran signed a ceasefire MoU.

- Three India-linked supertankers re-emerged in the Gulf of Oman, which suggests an increase in traffic through the waterway.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed with price action choppy following the recent conflicting headlines concerning US-Iran negotiations in Switzerland, as the Iranian delegation was said to have walked out of talks following Trump’s renewed threats to resume bombing them if a deal is not reached and if they don’t stop their proxies in Lebanon from causing trouble. However, the reports that gradually followed were more encouraging as mediators stated that talks were conducted in a positive, constructive atmosphere and technical talks are to continue for the remainder of the week, with the US and Iran agreeing to a de-confliction cell over Lebanon. Furthermore, the parties agreed to establish high-level committee to provide political oversight on mediation and on a roadmap to reach final deal within 60 days, while Iran’s Foreign Minister Araghchi confirmed that mediation delivered major progress to end the Lebanon war, as well as stated that oil and petrochem exports are waived, blockade is lifted, frozen assets released, and that a major reconstruction and development plan was launched for Iran. ASX 200 struggled for direction as strength in gold miners and financials was offset by weakness in tech, energy and defensives. Nikkei 225 extended on record highs and rallied firmly above the 72,000 level as exporters benefited from a weaker currency and a pullback in oil, although the index has pared some of the gains, but comfortably remained the outperformer. KOSPI swung between gains and losses amid a divergence between Samsung Electronics and SK Hynix, in which the latter took over the throne as South Korea’s largest Co. by market cap. Hang Seng and Shanghai Comp were mixed with sentiment not helped by trade frictions after China added 10 US firms to its export control list and announced to take relevant measures against 46 US companies in government procurement activities, while there was a lack of surprises from the announcement that the benchmark Loan Prime Rates were maintained for a 13th consecutive month.

Top Asian News

- The Japanese Government is reportedly planning to deploy JPY 68tln in public and private funding for the semiconductor sector by FY 2040, TV Asahi reported citing sources.

- Australia’s Agricultural Minister said testing has confirmed H5 bird flu detected in a second bird found in Western Australia.

- China’s Vice Premier Ding Xuexiang said risk of fragmented supply chains is growing and that some countries abuse use of export controls, adds China is anchor of stability and propeller of the global economy. said: Can work with all sides to build inclusive supply chains.

- Japanese Finance Minister Katayama ready to act suitably on currency fluctuations whenever necessary, but declines to comment on particular forex rates.

European bourses (STOXX 600 -0.2%) began the session on a muted footing, as markets digest the volatile geopolitical situation (see above). European sectors began the session mixed. Tech tops the pile with ASML +1.5% after it denied shipping EUV lithography machines, or any related component, to China, following US Commerce Secretary Lutnick’s accusations. Citi this morning wrote “we find it very hard to believe that they would jeopardise their position in the industry”. The sectoral laggard is Construction, one of its largest constituents Holcim -1.0% (9% weighting), after RBC downgraded Holcim’s PT, citing the completion of the acquisition of Xella and an update to Q2 results model

Top European News

- UK PM Starmer announces he will step down; nominations for Labour leader will open on 9th July, conclude by end-summer; will act as caretaker until new leader elected. Will fully support whoever takes over.

- UK PM’s Chief of Staff resigns, New Statesman reported.

- UK Minister Smith said “I would have been very happy for him to continue”, in reference to PM Starmer.

- UK Foreign Minister Cooper urges UK PM Starmer to resign, according to Sky News.

- Ireland said EU capital markets deal is possible by year end, according to FT.

- Italian PM Meloni called out US President Trump for “senseless”, “constant, unprovoked attacks”, while she said that Trump’s statements are completely made up and she doesn’t know why he behaves like this towards allies, after Trump told an Italian TV channel that Meloni begged him to take a picture with her and that he wouldn’t have taken it, but he felt sorry for her. Furthermore, Trump criticised Italy and its PM for not becoming involved with Iran and its nuclear threat.

FX

- DXY is firmer against all peers as it stabilises towards recent highs above 100. JPY is the underperformer after unsuccessful jawboning attempts, NOK holds on to gains after crude gapped higher at the re-open.

- USD-specific drivers are light, focus overnight was on geopolitics with US-Iran talks over the weekend whipsawing crude benchmarks. The main data point this week is PCE on Thursday, the session today sees remarks from Fed’s Waller, aside from this, the session is likely to be quiet and driven by geopolitical moves in oil/yields. DXY gapped higher at the APAC re-open and rose throughout the European morning to a peak of 101.01. Since this peak, the index has slipped and now more towards the unchanged mark.

- UK PM Starmer announces he will step down, remaining as a caretaker until a new leader is elected (Nominations begin on 9th July). Burnham is overwhelmingly considered as the front-runner, with GBP and Gilts seeing underperformance in recent weeks. There was no reaction to the announcement from Starmer himself, as it had been widely touted in recent days/weeks, especially following Burnham’s convincing victory in the Makerfield by-election. Given Burnham is nearly certain to become the next PM, focus is on his cabinet appointments, specifically his Chancellor pick. Over the weekend, the FT and Times made it clear that Miliband would be the least market friendly, citing comments from FTSE 100 executives; retaining Reeves would be the most market-friendly option, though the same outlets noted Burnham would likely want to remove the current Chancellor in a shift away from the last administration. GBP/USD -0.1% and tracking the stronger Buck. EUR/GBP +0.1%, gapped higher at the APAC re-open, but reversed most gains.

- JPY continues to underperform and moves further into intervention territory as USD/JPY looks towards 161.81 highs made last week. Japanese Finance Minister Katayama was on the wires overnight, said they were “ready to act suitably on currency fluctuations whenever necessary”; not sparking a move in the Yen. USD/JPY marked a session high of 161.78, looking to the aforementioned levels to the upside; awaiting further comments from Japanese officials.

- South African Parliamentary Speaker Didiza plans to support President Ramaphosa’s bid to halt his impeachment proceedings.

Central Banks

- Japan’s PM Takaichi said expect BoJ to closely coordinate with the government and conduct a monetary policy appropriately to achieve the 2% price goal.

- BoJ Deputy Governor Himino said takes some time for policy to have an impact on the economy. said:. Pass-through from oil prices to downstream goods has progressed somewhat rapidly. Recent easing of Middle East tensions doesn’t deviate much from their April outlook. Accommodative conditions are expected to continue. Risks of price overshoot could materialise if there is a delay in the necessary adjustment in the degree of monetary easing. Will closely monitor impacts that raising policy interest rates may have on businesses and households.

- ECB’s Escriva warns that rising oil and commodity prices linked to the Middle East conflict are feeding into consumer prices and could cause wage spillovers. said energy cost increases are already transmitting through areas such as transport services. ECB must monitor possible second-round wage effects depending on inflation persistence.

- Chinese Loan Prime Rate 1Y (Jun) 3.0% vs. Exp. 3.0% (Prev. 3.0%).

- Chinese Loan Prime Rate 5Y (Jun) 3.5% vs. Exp. 3.5% (Prev. 3.5%).

- SNB adjusts remuneration of sight deposits; lowering threshold factor from 15 to 13.5; effective August 1st 2026.

Fixed Income

- Fixed benchmarks are mixed. USTs in the red by around 10 ticks, but off a 109-07 trough by another five.

- USTs lower as a function of catch-up from the holiday session on Friday, and as the complex acknowledged the gap higher in energy at the resumption of trade after Iran seemingly shut Hormuz transit amid ongoing conflict in Lebanon. However, the updates from negotiators thereafter and as technical talks take place this week in Switzerland, points that allowed energy to retreat and gave relief to EGBs. USTs look ahead to remarks from Fed’s Waller.

- Bunds, as above, benefited from the energy retreat in the second half of the APAC session and are firmer by around 10 ticks, but a similar amount shy of the 126.34 high. Specifics light for the complex, no move to ECB commentary thus far, and we now await text from Lagarde at the ECON hearing.

- Additionally, Germany digests reports into another meeting of the pensions committee today. The main point from it being that the retirement age will increase, though not at the pace some have been seeking. More broadly, Politico reports budget progress, however, tax reform remains the major outstanding point.

- Last but not least Gilts, lower by 10 ticks and a similar amount of the low in 88.30-72 confines after gapping higher by 24 ticks, seemingly taking relief from numerous reports that the team around Burnham no longer saw Miliband as the favourite for Chancellor.

- Since, PM Starmer has resigned. He will serve as caretaker during the process which begins in three weeks and will last for no more than one week, 9th-16th July. Burnham is the clear favourite. However, the three weeks between now and the start of that process could potentially see the odds around Burnham and theoretical rivals, i.e. Streeting, change notably.

Geopolitics

- A very busy geopolitical weekend, which initially saw the Iranians shut the Strait of Hormuz, and it suggested that the US and Israel broke the interim ceasefire agreement amid the continued military strikes on southern Lebanon. This led Brent Aug’26 to gap higher by c. USD 2/bbl, to a session peak of USD 82.30/bbl. Attention then turned to US-Iran talks in Switzerland.

- The outcome of the initial talks were positive. A Qatari and Pakistani joint statement stated that US and Iran agreed to set up a de-confliction cell over Lebanon and agreed to establish a high-level committee to provide political oversight on mediation. The high-level committee also agreed to a roadmap to reach a final deal within 60 days.

- Following the positive mood music from the talks, Brent Aug’26 gradually moved off best levels and turned negative; currently lower by c. 1.1%, and at the bottom end of a USD 78.58-82.30/bbl range. Attention remains on further developments on the negotiation process, which is expected to continue throughout the week. For now, the heads of the delegation team have headed back to Iran, while technical teams will remain in Switzerland to follow up the implementation of the MoU.

- Spot gold (+0.8%) is in the green, benefiting from the disinflationary implications of the positive geopolitical mood music. XAU/USD is currently holding within a USD 4136-4221/oz range. On analyst commentary: Goldman Sachs expects central bank Gold buying to slow slightly but remain a structural floor for prices. GS forecasts central bank buying at roughly 50T a month in 2026, then slowing to around 40T a month in 2027.

- Base metals are broadly firmer this morning vs a mostly negative APAC session. Focus overnight remained on China adding US firms to its export control list and decided to take relevant measures against 46 US companies in government procurement activities. 3M LME Copper currently resides within a USD 13,598.28-13,736.93/t range.

- “Confirmed crossings through the monitored Strait of Hormuz zone rose sharply over 19–21 June, with 71 total transits recorded”, Kpler’s Bakr reported.

- Goldman Sachs expects central bank Gold buying to slow slightly but remain a structural floor for prices. GS forecasts central bank buying at roughly 50 T a month in 2026, then slowing to around 40 T a month in 2027.

- US Department of Agriculture announces three new cases of screwworm to take total number of domestic detections to 15 cases.

- Iraq asked operators of five major oil fields to boost output to pre-war levels, targeting output of more than 3mln bpd, while it was separately reported that Iraq intends to gradually increase oil production to between 4.2mln-4.3mln bpd, according to the deputy oil minister for upstream affairs.

- Qatar’s Interior Ministry reported an internal explosion at a factory in the Ras Laffan Industrial Area, although no injuries or leaks were reported.

- A fire occurred in Marathon Petroleum’s Galveston Bay refinery (631k bpd) but was extinguished.

- Guinea’s President Doumbouya announced a ban on raw gold exports, in an effort to boost local processing of the metal and help the domestic economy.

Trade/Tariffs

- Iranian delegation is set to travel to Tehran after talks in Switzerland.

- India’s Trade Minister said they intend to secure preferential market access via a trade agreement with the US. Signing of a US-India trade agreement will take longer than expected, because the US initially imposed 50% tariffs on Indian goods.

- China’s MOFCOM issues action plan on strengthening foreign Investment; to support qualified key foreign firms listing on domestic exchanges.

- China added 10 US firms to its export control list including USA Rare Earths, while the Finance Ministry announcing to take relevant measures against 46 US companies in government procurement activities.

- USTR Greer is to travel to India and Uzbekistan, while he will discuss the US-India joint statement as part of bilateral trade agreement talks.

US Event Calendar

- 9:00 am: Fed’s Waller Delivers Opening Remarks

DB’s Jim Reid concludes the overnight wrap

For those in Europe and parts of the US this week I hope you can cope with the expected extreme heat. The UK is certainly not ready for what’s about to hit us. I’m looking to exploit this and set up my own AI company. Aircon Installations. Please enquire for the best prices and for the IPO launching soon!

Talking of extreme heat, the latest developments out of the Middle East have turned more constructive after a highly volatile start to the weekend. Encouraging progress in US–Iran talks in Switzerland, mediated by Qatar and Pakistan, has seen both sides agree overnight to a roadmap towards a potential deal within 60 days, alongside the creation of technical working groups, a de conflict mechanism covering Lebanon, and a direct communication line aimed at avoiding incidents and keeping the Strait of Hormuz open. This marks a notable shift from Saturday’s confusion, when Iran suggested the strait was now closed again after Israeli attacks in Lebanon, and briefly stepped back from talks following renewed threats from President Trump, who reiterated that the US would strike again if Iranian-backed proxies in Lebanon continue attacks on Israel. Despite that rhetoric, oil flows through Hormuz have continued and even picked up over the weekend, helping to calm markets, with Brent reversing earlier gains this morning before details of the talks came through. What the overall positive weekend has perhaps taught us is that the path to a durable resolution remains fragile.

However, for now Brent crude (-1.61%) is reversing its earlier gains, currently trading at $79.27 per barrel. Asian equities are not seeing a clear trend with the Nikkei (+1.56%) notably higher, but with the KOSPI fairly flat after being up +2% earlier in the session. The Shanghai Comp is +0.18%, while the Hang Seng is down -0.98%. China’s central bank has maintained its benchmark lending rates for the 13th consecutive month overnight.

10-year USTs have increased by +3.2 bps, trading at 4.49% as cash trading has resumed following Friday’s US holiday. 2yr yields are +4.7bps. US equity futures are down around half a percentage point but that’s roughly where they were for a lot of Friday when the cash market was closed.

The main data highlights this week are the global flash PMIs tomorrow, and the US core PCE on Thursday. Elsewhere, other data of interest include the Ifo survey in Germany (Wednesday), Tokyo CPI in Japan (Friday), and CPI reports in Canada (today) and Australia (Wednesday). Note there is much speculation around whether UK Prime Minister Keir Starmer will resign this week after leadership rival Andy Burnham’s by-election win last week. The Observer newspaper yesterday reported that Starmer was preparing to set out a timetable for his departure, with an announcement possible today. If true it’s notable it’s happening on the eve of the 10th anniversary of the Brexit vote tomorrow, something the UK still hasn’t come to terms with. Since then, the UK has revolved through six Prime Ministers which alongside Brexit, underlines the immense difficulties many incumbents have in the Western World today. Everyone arrives in the post with great hopes but then the lack of growth and the financial realities hit. Until you have stronger economic growth and are less constrained by debt it’s highly likely the conveyor belt of PMs will continue.

On this, the Deutsche Bank Research Institute will be pleased to welcome you to our London offices on Thursday (11:30 refreshments for a 12-1 presentation) for a look at “Brexit 10 years on: Whats’s worked, what hasn’t, what’s next?”. I’ll be introducing Sanjay Raja and Shreyas Gopal in what looks set to be a fascinating week for the UK.

Moving over to the other side of the Atlantic, after a hawkish FOMC last week with a clear shift in style from new Fed Chair Kevin Warsh, our economists now have two 25bps hikes in their Fed forecast. They have warned that the US economy needed tighter policy but were waiting for the meeting to confirm the tightening view. The central scenario sees two rate increases this year, likely in September and December, taking the fed funds rate to around 4.1%, followed by a prolonged pause through 2027. Easing is then expected to resume in the first half of 2028, with around 50 basis points of cuts, potentially delivered in March and June, bringing policy back towards a neutral range of roughly 3.5–3.75%. See their piece explaining their view here.

In terms of the US week ahead, our economists expect appearances by Williams and Goolsbee on Thursday to be particularly informative. Williams, who also serves as Vice Chair of the FOMC, is seen as one of those not currently predicting a hike this year, while Goolsbee is viewed as leaning towards around 50 basis points of tightening.

Earlier that day, attention will centre on the data flow. US economists expect May personal income to rise by around 0.4% (from flat previously) and consumption to increase by 0.6% (from 0.5%). The core PCE deflator is projected to rise by around 0.37% month-on-month, up from 0.24%. On this basis, the year-on-year rate would move higher to approximately 3.44%, marking the strongest reading since October 2023 and reinforcing the narrative of persistent underlying inflation. The Fed will also release its bank stress test results on Wednesday and there is other second tier data.

Over in Europe, in addition to the PMIs, sentiment indicators in Germany will include the Ifo survey (Wednesday) and the July GfK consumer confidence print (Thursday). In France, there will be business confidence tomorrow and consumer confidence on Thursday. Finally, the ECB will release its May consumer expectations survey on Friday, with inflation expectations in focus. ECB speakers will include President Lagarde amongst others.

In Asia, inflation prints due include the Tokyo CPI for June on Friday in Japan (see our Chief Japan’s economist week-ahead here) and Australia’s May CPI due Wednesday (DB forecast for headline CPI is -0.4% MoM / 4.3% YoY). Other notable data features BoJ’s Summary of Opinions from its June meeting (Wednesday), Australia’s labour force survey (Thursday) and the 1-year and 5-year loan prime rates in China (Monday).

Finally, there will be a few notable earnings reports out next week, including FedEx, Cerebras and Carnival tomorrow as well as Micron and Jefferies on Wednesday. Micron is up around 830% over the last year and around 250% since the end of March with a market cap of nearly $1.3tn. So it’s becoming one to follow from the macro side.

Recapping last week, oil prices kept falling as they reacted to the news that the US and Iran had reached an interim deal. So that meant Brent crude fell -7.74% last week (+0.90% Friday) to $80.57/bbl. So that considerably eased fears about a stagflationary shock to the global economy, particularly as data showed more traffic was starting to flow through the Strait of Hormuz again. Indeed, near-term inflation expectations plummeted, with the 1yr US inflation swap down -30.8bps last week to 2.44%, whilst the 1yr Euro inflation swap was down -23.7bps to 2.60%.

But even as inflation expectations fell, the Fed’s latest decision on Wednesday led to a clear hawkish repricing for markets. Notably, 9 of the 18 officials in the dot plot signalled there should be a rate hike this year, although new Chair Kevin Warsh did not submit a dot himself. But Warsh did reiterate the Fed’s inflation target, pledging to return inflation to target after five years above. Meanwhile in Japan, the Bank of Japan delivered a 25bp rate hike, taking their policy rate to a post-1995 high of 1%.

That backdrop meant markets brought forward their expectations for a Fed rate hike. So by the end of the week, 39bps of Fed hikes were priced in by December, up from 21bps at the start of the week. In turn, that led to a flattening in the Treasury yield curve, with the 2yr Treasury yield up +9.6bps to 4.18%, whilst the 10yr yield (-2.6bps) fell to 4.45%. A similar pattern was evident globally, with Germany’s 2yr yield (+2.7bps) up to 2.64%, whilst the 10yr yield (-1.0ps) fell to 2.98%.

Whilst equities saw a pullback after the Fed decision, they still ended the week higher as concern about a stagflationary shock faded. So the S&P 500 was up +0.93%, Europe’s STOXX 600 was up +0.38%, and Japan’s Nikkei surged by +7.92%, marking its biggest weekly jump since August 2024. The moves were supported by the ongoing rebound in chip stocks, with the Philly semiconductor index up +7.26% to a new record.

Recapping last week now and oil prices kept falling as they reacted to the news that the US and Iran had reached an interim deal. So that meant Brent crude fell -7.74% last week (+0.90% Friday) to $80.57/bbl. So that considerably eased fears about a stagflationary shock to the global economy, particularly as data showed more traffic was starting to flow through the Strait of Hormuz again. Indeed, near-term inflation expectations plummeted, with the 1yr US inflation swap down -30.8bps last week to 2.44%, whilst the 1yr Euro inflation swap was down -23.7bps to 2.60%.

But even as inflation expectations fell, the Fed’s latest decision on Wednesday led to a clear hawkish repricing for markets. Notably, 9 of the 18 officials in the dot plot signalled there should be a rate hike this year, although new Chair Kevin Warsh did not submit a dot himself. But Warsh did reiterate the Fed’s inflation target, pledging to return inflation to target after five years above. Meanwhile in Japan, the Bank of Japan delivered a 25bp rate hike, taking their policy rate to a post-1995 high of 1%.

That backdrop meant markets brought forward their expectations for a Fed rate hike. So by the end of the week, 39bps of Fed hikes were priced in by December, up from 21bps at the start of the week. In turn, that led to a flattening in the Treasury yield curve, with the 2yr Treasury yield up +9.6bps to 4.18%, whilst the 10yr yield (-2.6bps) fell to 4.45%. A similar pattern was evident globally, with Germany’s 2yr yield (+2.7bps) up to 2.64%, whilst the 10yr yield (-1.0ps) fell to 2.98%.

Whilst equities saw a pullback after the Fed decision, they still ended the week higher as concern about a stagflationary shock faded. So the S&P 500 was up +0.93%, Europe’s STOXX 600 was up +0.38%, and Japan’s Nikkei surged by +7.92%, marking its biggest weekly jump since August 2024. The moves were supported by the ongoing rebound in chip stocks, with the Philly semiconductor index up +7.26% to a new record.

Tyler Durden

Mon, 06/22/2026 – 08:26